Banking Software Development Services: Complete Guide for Financial Institutions

Banking software development services help financial institutions build secure, compliant, scalable platforms for core banking, digital banking, risk management, integrations, and customer engagement. For banks evaluating modernization, the goal is not simply to replace old technology; it is to streamline operations, reduce operational costs, protect financial data, and create better customer experience across every banking channel.

Banking software development includes custom financial software development for core banking systems, mobile banking apps, web portals, account management, transaction processing, compliance automation, fraud detection systems, data analytics, CRM systems, and integration engines. It does not usually include generic fintech apps with no regulated banking context, hardware procurement, telecom infrastructure, or non-financial sector software. The distinction matters because banking software must align with security needs, compliance mandates, and long-term business goals.

This guide is for banking executives, CIOs, CTOs, compliance leaders, architecture teams, and financial service decision-makers evaluating secure software modernization. It is also relevant to financial services companies comparing a banking software development company, a financial software development company, or an internal financial software development team for platform transformation.

In practical terms, banking software development services create secure, compliant, and scalable custom software solutions that automate banking operations, integrate legacy banking systems, improve operational efficiency, and enhance customer satisfaction. Specialized banking software development services offer unique advantages such as built-in regulatory compliance, superior security measures, and a deep understanding of the financial services industry that general software development providers often lack.

By the end of this guide, you will understand:

The main types of banking software solutions, including core banking, transaction processing, CRM, and compliance platforms.

How implementation works across planning, architecture, development, testing, deployment, and ongoing support.

Why regulatory compliance, data security, and security testing must be embedded into the software development lifecycle.

How to evaluate integrations, open APIs, cloud solutions, and platform control.

Which ROI metrics matter, including operational efficiency, customer acquisition, uptime, processing speed, and audit readiness.

For broader modernization context across banking services, see our banking industry software overview.

Understanding Banking Software Development

Banking software development is the design, engineering, deployment, and support of software solutions built specifically for financial institutions. Unlike generic software development, software development financial services work must account for sensitive data, financial transactions, concurrency, auditability, regulatory reporting, and high availability from the beginning.

Custom banking software development focuses on creating tailored solutions that meet the specific operational needs of financial organizations, improve customer service, and ensure data security. These solutions may support account management, payments, lending, customer onboarding, risk management, back office operations, and digital customer engagement. The benefits of custom banking software development include enhanced customer experience through personalized services, improved data management, and the ability to scale operations effectively as business needs evolve.

Banking software development is especially relevant now because legacy systems often limit scalability and innovation. Many financial institutions still depend on legacy banking systems built around monolithic architectures, batch processing, or outdated vendor constraints. Legacy system modernization is crucial for integrating new applications with traditional banking systems, and modernization of legacy systems can improve performance, security, maintainability, and usability, which are critical for meeting the evolving demands of the banking sector.

Modernization is also a business outcome issue. Banks can achieve significant operational efficiency by automating routine processes, reducing manual intervention, and minimizing errors, leading to increased productivity. Streamlining back-office operations through digital banking solutions can enhance operational efficiency by enabling banks to make informed business decisions and minimize financial risks.

Core Banking Systems

Core banking systems are the foundational banking systems that manage customer accounts, deposits, withdrawals, balances, interest calculations, transaction posting, and general ledger activity. In most institutions, core banking is the system of record for financial operations and customer data.

These platforms sit at the center of banking operations. Every mobile transfer, card payment, account update, loan repayment, or customer service interaction ultimately depends on core banking data being accurate, available, and secure. Financial applications require high availability and instantaneous transaction processing, ensuring concurrency in financial operations even during peak usage.

For many banks, core modernization means moving from rigid, tightly coupled platforms toward flexible, cloud-native architectures. The transition to cloud-native architectures is essential for modernizing core banking systems because it helps banks minimize operational complexity, support sustainable long-term growth, and handle increasing transaction volumes without performance degradation.

Digital Banking Applications

Digital banking applications are customer-facing software products such as mobile banking apps, web banking portals, desktop interfaces, onboarding tools, self-service features, and digital engagement platforms. Banking software must provide an omnichannel user experience across mobile apps, web portals, and desktop interfaces so customers can begin a process in one channel and complete it in another without friction.

Digital banking applications only work well when they are tightly integrated with backend infrastructure. A balance shown in a mobile app, a payment initiated through a web portal, or a support request handled by a chatbot must connect reliably to core banking systems, payment gateways, compliance checks, and customer data platforms.

Upgrading legacy systems is crucial for banks to enhance customer experience, because outdated technology can lead to slow, cluttered, and insecure banking operations that drive customers away. Open banking initiatives, which leverage APIs, are also crucial for creating a dynamic ecosystem that meets regulatory demands and customer expectations while facilitating seamless integration with third-party providers.

Together, core banking systems and digital banking applications define the foundation. The next step is understanding the specific software types that sit around that foundation and enable secure, modern banking services.

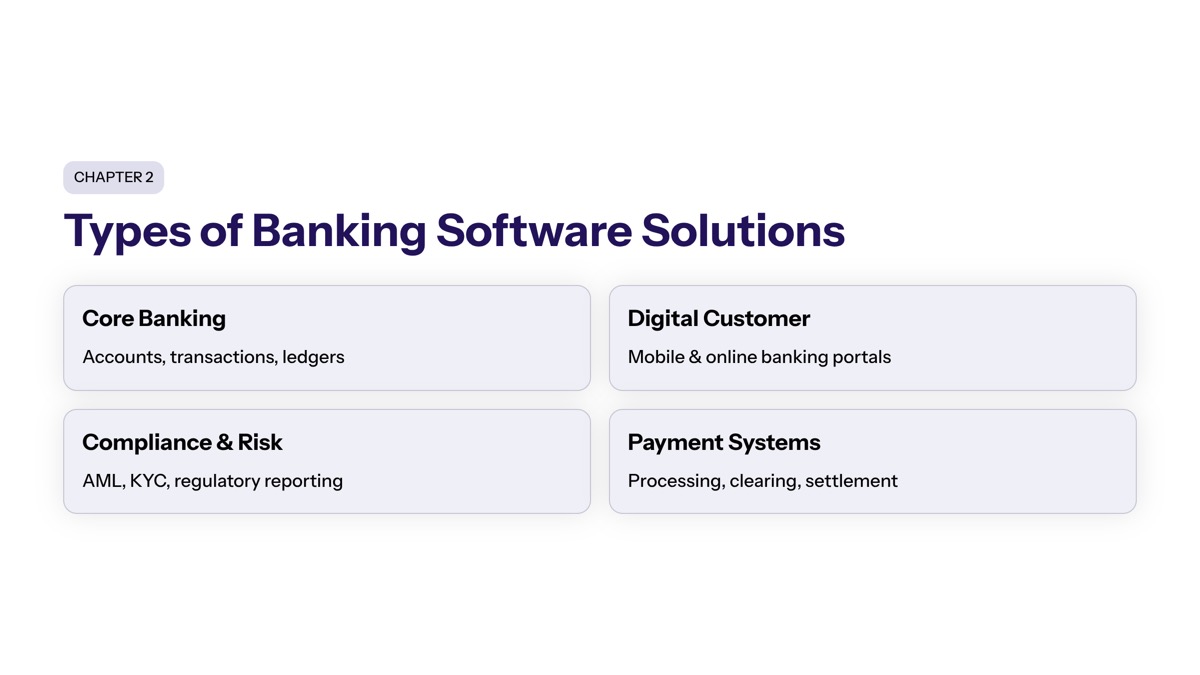

Types of Banking Software Solutions

Modern banking software is not a single application. It is an ecosystem of financial software systems that connect customer channels, core ledgers, compliance workflows, risk tools, analytics platforms, and third-party services. A well-designed banking software platform should feature open APIs to facilitate integration and support long-term platform control.

Banking leaders should think in terms of business capabilities rather than isolated applications: transaction execution, regulatory control, customer engagement, operational insight, and scalable integration. The right mix of financial software solutions depends on institution size, regulatory environment, product complexity, and modernization maturity.

Transaction Processing Systems

Transaction processing systems handle the movement of money across accounts, cards, payment rails, settlement networks, clearing systems, and internal ledgers. In banking software, transaction processing includes authorization, posting, settlement, reconciliation, and transaction monitoring.

High-volume transaction processing necessitates specific architectural choices like microservices, event streaming, API gateways, and resilient data stores. Scalable banking software must handle increasing transaction volumes without performance degradation, while preserving audit trails and data consistency.

Legacy cores often rely on end-of-day batch processing, while modern digital banking software increasingly requires real-time or near-real-time updates. AFC Bank in Zimbabwe, for example, completed a full digital core modernization that reduced end-of-day processing time by 94%, from approximately 8 hours to around 30 minutes, while achieving 90 transactions per second. The same modernization migrated over 50,000 customers and supported more than 30,000 transactions and 200,000 digital inquiries daily.

Transaction monitoring is also part of modern payment architecture. AI-driven automation in banking enhances fraud detection by using machine learning algorithms to analyze transaction patterns and identify anomalies in real time, significantly reducing the risk of fraudulent activities.

Risk Management and Compliance Platforms

Risk management and compliance platforms support AML, KYC, fraud detection, sanctions screening, regulatory reporting, audit logging, credit risk analysis, and operational risk controls. These platforms connect directly to core banking operations because compliance decisions often depend on customer identity, transaction history, account behavior, and payment context.

Regulatory compliance is essential in banking software development, as financial institutions must adhere to various regulations such as PCI DSS, GDPR, and local banking laws to protect sensitive data and maintain customer trust. Automating compliance checks for regulations like AML and KYC helps financial institutions reduce legal risks and prepare for audits more effectively, ensuring ongoing adherence to industry standards.

Financial software developers must design these platforms for traceability. Compliance teams need immutable audit trails, configurable rules, data lineage, role-based approvals, and reporting outputs that can withstand regulator scrutiny. ISO 20022, SWIFT standards, PSD2, open banking, PCI DSS, GDPR, CCPA, SOX, and local banking laws all influence how banking software solutions are architected.

AI and advanced analytics are becoming increasingly important in this category. AI technologies in banking enable data-driven decision-making by providing predictive insights and real-time analytics, allowing banks to adjust strategies based on customer behavior and market trends.

Customer Relationship Management

Customer relationship management in banking includes CRM systems, customer analytics, segmentation, personalization engines, campaign tools, service dashboards, and customer engagement workflows. These systems help banks improve customer satisfaction, retention, cross-sell relevance, and customer acquisition.

Personalized user experiences in banking can be enhanced through data analytics and machine learning capabilities. Financial institutions are increasingly adopting AI-driven automation to improve customer service through personalized experiences, using chatbots and predictive analytics to address customer inquiries and needs more efficiently.

A strong banking CRM must integrate with customer data, account data, product data, communication history, consent preferences, and transaction behavior. Implementing advanced data analytics in banking software allows institutions to track key performance indicators in real time, facilitating faster and smarter operational decisions.

The key integration requirement is consistency: transaction processing systems, compliance platforms, and CRM systems must share reliable data without creating privacy risks or conflicting records. That is why system architecture for banking software should support integration with existing core banking systems, third-party payment gateways, and fintech tools.

Banking Software Development Implementation

Implementation is where strategy becomes risk management. Banking software development services must combine software engineering discipline, financial technology expertise, project management, compliance governance, and operational continuity.

Successful banking software development requires deep domain expertise in financial technologies rather than general software development experience. The development process for custom banking software typically involves planning and requirements gathering, design and architecture, development and testing, and ongoing maintenance to ensure compliance and security. In a regulated environment, each step must preserve customer trust, data security, auditability, and service availability.

Development Methodology and Process

A structured development approach is essential when banks develop financial software, modernize core systems, or integrate new digital banking capabilities with legacy platforms. The process should be iterative enough to deliver value and controlled enough to satisfy regulatory compliance, security, and operational risk requirements.

Requirements analysis and compliance mapping

Identify business goals, customer journeys, product rules, transaction volumes, non-functional requirements, integration dependencies, and regulatory obligations. This stage should map AML, KYC, PCI DSS, GDPR, local banking laws, ISO 20022, and open banking requirements where relevant.Security-first architecture design

Define identity and access management, encryption, secrets management, audit trails, network segmentation, API governance, and deployment environments. Ideal banking software must align with security needs, compliance mandates, and long-term business goals, not only near-term feature delivery.Agile development with regulatory checkpoints

Build in sprints while involving compliance, risk, security, operations, and business stakeholders throughout delivery. Security testing should be embedded in each stage of the software development lifecycle to ensure that banking applications are resilient against cyber threats and vulnerabilities.Comprehensive testing and validation

Use unit testing, integration testing, performance testing, penetration testing, vulnerability scanning, data migration rehearsals, and user acceptance testing. For financial transactions, testing must validate concurrency, rounding rules, ledger accuracy, latency, and exception handling.Staged deployment and monitoring

Use phased rollouts, blue-green deployments, canary releases, feature flags, and rollback plans where possible. Envadel’s modernization of a mid-size European bank with more than 2 million customers used domain-driven microservices, Kubernetes, and Kafka event streaming; over 14 months, the project delivered 70% faster deployment lead time while maintaining 99.99% uptime during migration.Ongoing maintenance and updates

Provide ongoing support for security patches, regulatory updates, performance tuning, feature extensions, documentation, and third-party integration lifecycle management. Custom banking software can significantly improve operational efficiency by automating repetitive tasks, minimizing manual intervention, and providing real-time data analytics for informed decision-making, but those gains must be protected after launch.

Technology Stack Comparison

Technology choices determine how much control, scalability, security, and compliance flexibility a bank will have over time. Cloud solutions, hybrid infrastructure, and legacy integration platforms can all be valid depending on regulatory constraints, risk appetite, existing architecture, and modernization roadmap.

Technology Stack | Security Level | Scalability | Compliance Support |

|---|---|---|---|

Cloud-native solutions | High when designed with encryption, identity controls, secrets management, network isolation, monitoring, and automated security testing. | Very high; microservices, containers, event streaming, and elastic infrastructure support real-time data processing and growth. | Strong; cloud-based banking solutions enhance scalability, reduce infrastructure costs, improve data security, and enable real-time data processing, which collectively improve decision-making and customer service. |

Hybrid infrastructure | High, but more complex because banks must secure cloud, on-premises, private cloud, and integration boundaries. | Moderate to high; cloud components can scale while sensitive workloads remain under tighter institutional control. | Good for data residency and regulatory constraints, though auditability and governance must be consistent across environments. |

Legacy integration platforms | Variable; older systems may lack modern encryption, identity management, automated testing, and observability. | Limited; scaling often depends on hardware, vendor cycles, custom patches, and batch-oriented processing. | Mixed; existing certifications may help, but adapting to new regulatory demands can be slow and costly. |

For banks with heavy regulatory requirements, hybrid and cloud-native architectures often provide the best balance of control and adaptability. Legacy systems integration may still be necessary during transition, but the long-term goal should be modularity, open APIs, event-driven data flows, and clear ownership of platform capabilities.

Kotak Mahindra Bank’s core banking replacement illustrates the scale of integration planning required. The bank completed a big-bang Finacle implementation across 340 branches, approximately 2 million customers, and 4 million accounts, integrating 72 systems. ATM uptime remained intact, other channels experienced approximately 30 hours of downtime, and the solution was designed for more than 99.99% uptime. After go-live, new account openings rose 44% in the quarter.

Common Challenges and Solutions

Banking modernization programs fail when they underestimate legacy complexity, compliance effort, integration volume, data quality, or organizational change. Development services for the financial sector must reduce these risks with governance, architecture discipline, and measurable business outcomes.

The most effective banking software development programs treat modernization as a controlled platform transformation. That means building robust software solutions that protect sensitive data, improve financial processes, and give the institution more control over future change.

Legacy System Integration

Legacy system integration is difficult because older platforms often contain undocumented business rules, fragmented customer data, batch dependencies, and one-off connections to reporting tools, payment processors, and back office operations. In some migration programs, timelines initially planned for 12 months have stretched to 28 months because data mapping, hidden logic, and integration dependencies were underestimated.

The solution is an API-first integration strategy supported by domain-driven design, event streaming, change data capture, and staged replacement. A well-designed modernization program can wrap legacy functionality with APIs, isolate high-risk components, and gradually replace them using a strangler pattern rather than forcing every system into a single risky cutover.

Modernization of legacy systems can improve performance, security, maintainability, and usability. It also gives banks a path to flexible, cloud-native architectures that support customer engagement, real-time financial operations, and integration with fintech tools.

Regulatory Compliance Requirements

Compliance risk is one of the main reasons banks need specialized financial services software development. Generic software solutions may handle workflows, but banking solutions must produce regulator-ready evidence: audit trails, access logs, approval histories, data lineage, retention controls, and policy enforcement.

The solution is compliance by design. Compliance requirements should be mapped during discovery, converted into architecture and workflow controls, tested during delivery, and monitored after launch. Automated audit trails and automated compliance checks for AML and KYC reduce legal risks, improve audit preparation, and support ongoing adherence to industry standards.

A mature banking software development company should understand PCI DSS, GDPR, SOX, AML/KYC rules, ISO 20022, SWIFT messaging, open banking expectations, and local banking laws. The aim is not just passing an audit; it is building financial software systems that can adapt as regulation changes.

Data Security and Privacy

Data security and privacy risks include breaches, unauthorized access, insider threats, insecure APIs, weak encryption, data residency violations, and poor handling of sensitive data. These risks are amplified in banking because financial data, customer data, identity records, and transaction histories are high-value targets.

The solution is layered security: encryption at rest and in transit, least-privilege access, multi-factor authentication, role-based controls, separation of duties, secrets management, continuous monitoring, vulnerability scanning, penetration testing, and incident response planning. Security testing should remain embedded throughout the software development lifecycle rather than treated as a final pre-launch task.

Banks should also use data anonymization or pseudonymization where appropriate, strict retention policies, SIEM monitoring, and clear governance over third-party access. When data security is engineered into the platform, banks reduce operational risk while improving trust in digital banking, mobile banking apps, and integrated banking services.

Conclusion and Next Steps

Banking software development services are most valuable when they create measurable business outcomes: stronger compliance, faster product delivery, lower operational costs, better customer satisfaction, secure integrations, and greater platform control. For financial institutions, modernization is no longer only an IT initiative; it is a strategic capability for competing in the financial services industry.

A successful program depends on choosing the right architecture, the right sequencing, and the right development partner. Custom software can provide differentiation, but only when it is governed carefully, integrated cleanly, and supported over time. Vendor platforms can accelerate delivery, but only when configuration, APIs, data ownership, and upgrade paths are understood.

Recommended next steps:

Assess current system architecture and compliance gaps

Review legacy systems, integration points, data quality, security controls, audit findings, and regulatory obligations.Define digital banking strategy and priority initiatives

Identify which outcomes matter first: operational efficiency, mobile banking apps, customer acquisition, fraud detection, account management, or back office automation.Evaluate development partners with banking expertise

Look for financial software development services with proven banking industry experience, security credentials, integration capability, and a deep understanding of compliance.Plan a phased implementation approach

Prioritize high-value modules, reduce cutover risk, define rollback plans, and track KPIs such as uptime, transaction latency, deployment lead time, incident rate, audit readiness, and customer satisfaction.

Related topics worth exploring include AI integration in banking, open banking APIs, and cloud migration strategies. Each one extends the same modernization theme: better data control, faster decision-making, stronger compliance, and more adaptable banking software.

Additional Resources

Use the following reference areas when evaluating banking software development services, financial software solutions, or a banking software development company.

Regulatory compliance frameworks

PCI DSS, SOX, GDPR, CCPA, AML/KYC rules, local banking laws, data residency requirements, and privacy regulations.Banking technology standards

ISO 20022, SWIFT standards, SWIFT CBPR+, SEPA for European payments, open banking standards, PSD2, Basel frameworks, and risk reporting requirements.Vendor evaluation checklist

Assess banking domain expertise, security certifications, compliance knowledge, architecture approach, API strategy, cloud and hybrid experience, data migration capability, third-party integration history, project management maturity, support model, and total cost of ownership.Architecture checklist

Confirm support for open APIs, microservices where appropriate, event-driven processing, observability, automated testing, encryption, identity management, audit trails, regulatory reporting, and integration with existing core banking systems, third-party payment gateways, and fintech tools.ROI metrics to track

Operational costs, deployment velocity, transaction processing speed, uptime, mean time to recovery, number of production incidents, digital adoption, new account growth, regulatory reporting accuracy, fraud reduction, and customer satisfaction.