Budgeting Transformation: Where Money Actually Moves the Needle?

“Budgeting transformation” becomes real the moment you stop funding initiatives and start funding measurable outcomes.

In RAPID terms, the point of the work is to align actions around specific measurable outcomes—not vanity metrics—and then make decisions that keep momentum moving. That includes budget decisions. Because if the plan isn’t funded, it was never a plan—just a document.

Ali Davachi makes this painfully concrete: a company can agree it “should” hire a digital marketer, but if that decision never makes it into the budget, the plan fails from the start. Same story with missing licenses: momentum was short-circuited because essential resources weren’t provided in time.

This post shows how to do budgeting transformation the RAPID way: link spend to outcomes, expose bottlenecks, reduce waste, and invest where money actually moves the needle.

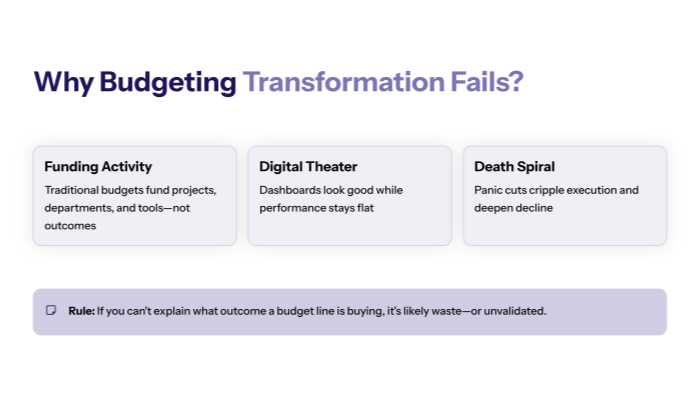

Why budgeting transformation fails in the real world?

1.1 The most common failure: funding activity instead of outcomes

Traditional budgeting often funds:

- projects (deliverables, timelines)

- departments (headcount quotas)

- tools (“we need a new platform”)

RAPID pushes the opposite logic: outcomes power everything, and the process exists to remove doubt by aligning action around measurable outcomes instead of vanity metrics.

If your budgeting transformation isn’t tied to outcomes, it drifts into:

- “digital transformation” theater

- internal politics (“my initiative matters more”)

- dashboards that look good while performance stays flat

Rule: if you can’t explain what outcome a budget line is buying, it’s likely waste—or at least unvalidated.

1.2 The silent killer: “budget slashing” that triggers a death spiral

RAPID calls out a pattern: leaders under pressure start cutting left and right (people, product lines, facilities) just to stay a going concern—then the cuts cripple the company and deepen the decline.

Budgeting transformation isn’t “spend more.” It’s:

- cut what doesn’t move outcomes

- protect and fund what removes constraints

- avoid self-inflicted wounds that reduce your ability to execute

This is why sequencing and measurement matter: you don’t guess where to cut or invest—you prove it.

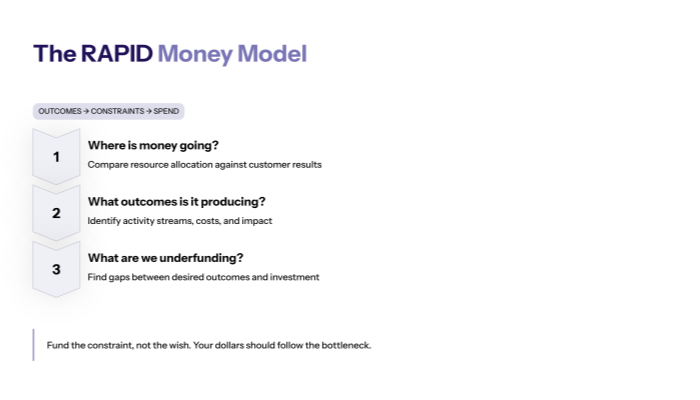

The RAPID money model (Outcomes → Constraints → Spend)

2.1 Budgeting transformation starts with allocation vs customer results

RAPID’s “Financial Analysis” is straightforward: compare and contrast how resources are allocated against customer results, then identify activity streams, costs, and their impact on desired outcomes.

That is the core of budgeting transformation:

- Where is the money going today?

- What outcomes is it producing?

- What outcomes are we not funding enough to achieve?

It also forces uncomfortable truth: a company can be pursuing results but not putting enough money toward them to create success.

2.2 Fund the constraint, not the wish

RAPID’s flywheel logic matters here: Research/Analyze surfaces the real bottleneck, then Plan/Implement/Decide allocates action (and resources) to remove it and adapt based on results.

Budgeting transformation means your dollars should follow the constraint:

- if decision latency is the constraint → fund decision rights redesign, escalation SLAs, lightweight governance

- if rework is the constraint → fund intake standardization, QA, definition-of-done

- if data trust is the constraint → fund reconciliation, metric definitions, reporting pipelines

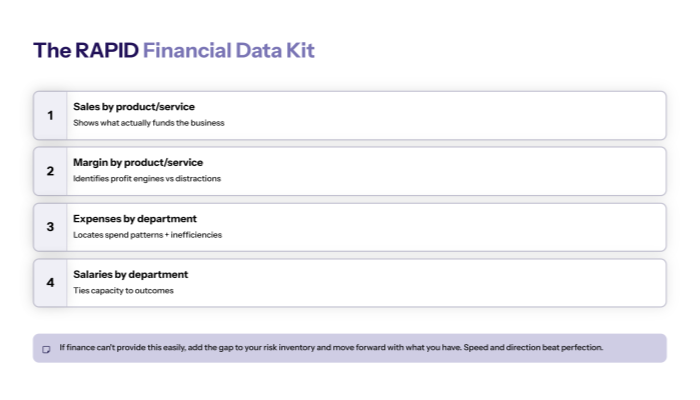

What to measure and request? (the RAPID financial data kit)

3.1 Use RAPID Financial Research to get directional data fast

RAPID includes a dedicated tool: (R) Financial Research—ask finance for high-level data (mostly from the P&L) broken down by month, for directional analysis later.

Here’s the RAPID request list you can reuse:

Data request |

Why it matters for budgeting transformation |

|---|---|

Sales by product/service |

Shows what actually funds the business |

Sales by customer (ideally by product/service) |

Reveals concentration risk + where value is created |

Margin by product/service |

Identifies profit engines vs distractions |

Margin by customer |

Shows which customers are worth serving |

Expenses by department |

Locates spend patterns + inefficiencies |

Salaries by department (rough is fine) |

Ties capacity to outcomes |

Internal financial/ops KPIs tracked |

Reveals what leadership “steers” by today |

If finance can’t provide this easily, RAPID advises adding the gap to your risk inventory/product gaps and moving forward with what you have. The goal is speed and direction, not perfection.

3.2 If data isn’t timely and shared, governance becomes guesswork

RAPID makes a hard point: if a company can’t get timely, accurate financial data and share it transparently and appropriately with decision makers, major issues are inevitable.

Budgeting transformation depends on shared truth:

- consistent reporting definitions

- consistent refresh cadence

- visibility across decision makers

Even “simple” issues (like time zone timing on reports) can fracture alignment if leaders compare numbers that aren’t actually comparable.

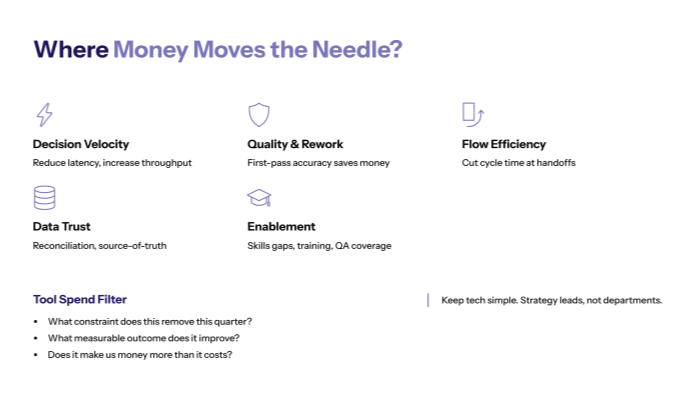

Where money actually moves the needle?

4.1 Spend categories that typically produce real transformation returns

RAPID repeatedly points you to the practical levers: people, process, product—then obtain the resources needed to execute. Budgeting transformation should prioritize spend that reduces friction and increases outcome throughput.

High-leverage buckets:

- Decision velocity (reduce latency)

- Quality & rework reduction (first-pass accuracy)

- Flow efficiency (cycle time, queue time at handoffs)

- Data trust (reconciliation, source-of-truth)

- Enablement (skills gaps, training, QA coverage)

RAPID gives a simple illustration: if you have X developers, you likely need Y QA—because investing in product without investing in quality is misallocation.

4.2 Tool spend: keep it simple and make sure strategy leads

RAPID’s guidance on IT is blunt:

- “If tech is involved, keep it simple.”

- Leadership should dictate strategy—not a department.

- Technology should support the company, not the company supporting technology (“tail wagging the dog”).

So budgeting transformation should treat tools as constraint solvers, not identity statements.

A simple filter for software spend:

- What constraint does this remove this quarter?

- What measurable outcome does it improve?

- Does it make us money (or reduce cost-to-serve) more than it costs?

If the answer is unclear, the tool is likely a distraction.

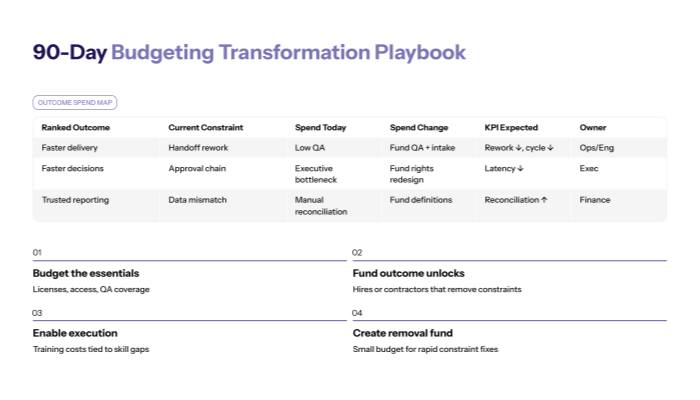

A 90-day budgeting transformation playbook

5.1 The “Outcome Spend Map” (table you can run in one meeting)

Use this to turn budgeting transformation into a repeatable operating step.

Ranked outcome |

Current constraint |

Spend today |

Spend change (90d) |

KPI you expect to move |

Owner |

|---|---|---|---|---|---|

Faster delivery |

Handoff rework |

Low QA / unclear intake |

Fund QA coverage + intake standard |

Rework rate ↓, cycle time ↓ |

Ops/Eng |

Faster decisions |

Approval chain |

Executive bottleneck |

Fund decision rights redesign |

Decision latency ↓ |

Exec sponsor |

Trusted reporting |

Data mismatch |

Manual reconciliation |

Fund metric definitions + pipeline |

Reconciliation rate ↑ |

Finance/Data |

This is exactly what RAPID’s financial analysis is for: identify activity streams and costs, and connect them to outcome impact.

5.2 Protect momentum: budget the decisions (and the essentials)

RAPID warns that momentum dies when essential resources aren’t provided in time—like licenses that were promised but never delivered. And it gives the clearest budgeting lesson in the book: a plan can fail simply because the decision never got put in the budget.

So in your 90-day budgeting transformation plan, explicitly budget:

- the essentials required to execute (licenses, access, QA coverage)

- the hires or contractors that unlock outcomes

- enablement/training costs tied to skill gaps

- a small “constraint removal fund” for rapid fixes discovered during implementation

Then keep the PID flywheel moving: plan → implement → decide based on results, and adapt without fear of being wrong.

Final takeaway

Budgeting transformation isn’t “cost control.” It’s outcome control.

RAPID gives you the logic:

- measure what outcomes matter (not vanity metrics)

- identify constraints beneath the surface

- compare resource allocation to customer results

- fund what removes the bottleneck and protects momentum

- keep tech simple and strategy-led