Fervo Energy’s IPO Reveals AI Data Centers Are Transforming U.S. Energy Demand

Fervo Energy’s May 2026 initial public offering marks a defining moment in how artificial intelligence is reshaping American energy infrastructure. The company is preparing to raise approximately $1.33 billion through public markets under the FRVO ticker, signaling that enhanced geothermal systems have moved from experimental technology to grid-scale investment thesis. This IPO represents more than a single company going public—it reflects a fundamental shift in how energy markets value reliable, carbon-free electricity generation.

This article examines the connection between AI computational requirements, the limitations of traditional renewables, and why geothermal energy has emerged as a critical solution for technology companies. The scope covers technical aspects of enhanced geothermal development, market dynamics driving investor interest, and practical implications for energy infrastructure planning. Enterprise technology leaders, energy investors, and infrastructure decision-makers evaluating clean energy partnerships will find actionable insights for navigating this transformation.

Fervo’s IPO valuation—targeting a market value of up to $7.37 billion—reflects investor confidence that AI data centers require 24/7 carbon-free power that unlike solar and wind farms, geothermal can deliver continuously. The IPO’s valuation implies a successful bet on the next-generation geothermal cycle, which includes converting a $7.2 billion potential backlog of contracted revenue into profitable assets.

By the end of this article, you will understand:

-

Why AI power consumption patterns differ fundamentally from traditional computing

-

How intermittent renewable sources fail to meet data center reliability requirements

-

What makes Fervo’s enhanced geothermal approach technically and economically viable

-

The market implications for energy infrastructure investment and corporate energy procurement

-

Strategic considerations for organizations planning data center development

Understanding AI Data Center Energy Requirements

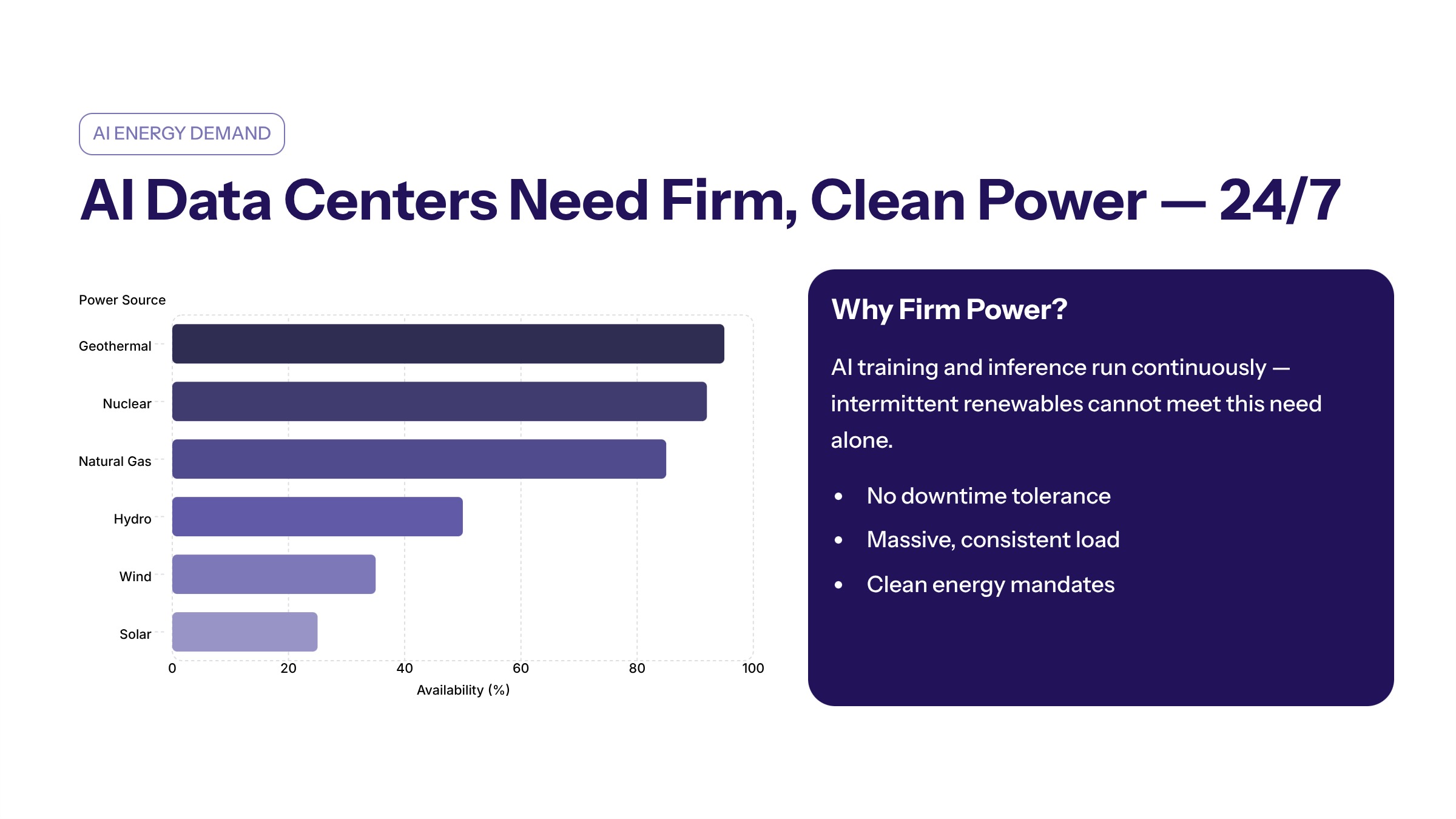

AI data centers demand continuous, high-capacity power, requiring a shift from traditional energy sources to firm, 24/7 carbon-free electricity. This fundamental requirement is driving a restructuring of how technology companies approach energy procurement and infrastructure planning.

Continuous Power Demand vs. Traditional Computing

AI workloads operate differently from conventional data center operations. Training large language models and running inference at scale requires sustained, intensive computational cycles that cannot tolerate power interruptions. The projected electricity consumption from data centers could reach nearly 9% of total U.S. electricity by 2030 due to AI’s growing requirements.

Power density compounds these challenges. A five-acre facility transitioning from standard computing to AI workloads can see electricity demand jump from approximately 5 megawatts to 50 megawatts. Current server racks draw around 130 kilowatts, with projections reaching 600 kilowatts by 2027 and potentially 1 megawatt per rack by decade’s end. This concentration of demand creates unprecedented infrastructure requirements.

Grid Reliability and Carbon Commitments

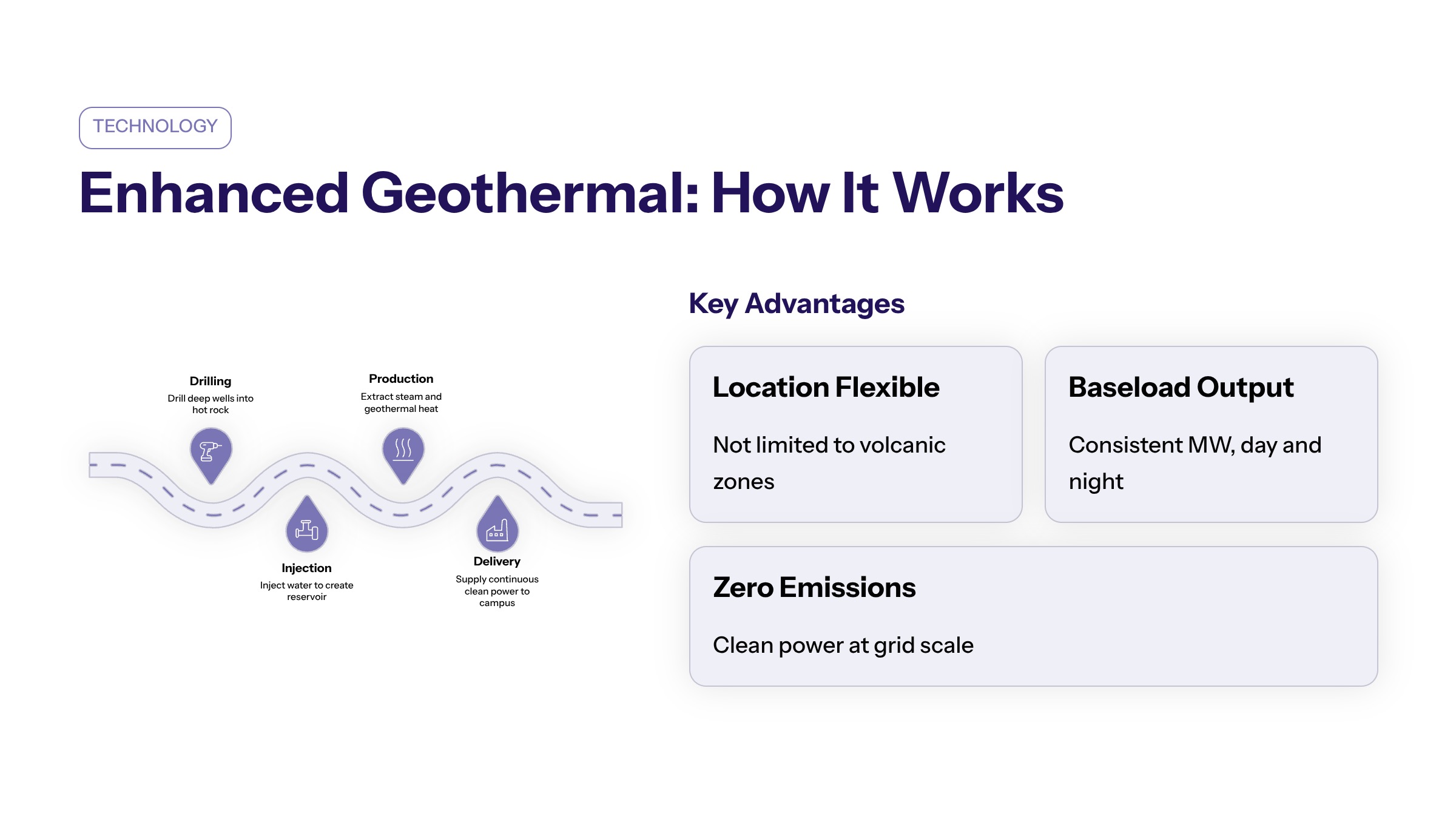

Tech companies face dual pressures: ensuring uptime while meeting net-zero commitments. The demand for AI data centers is creating a strong need for reliable, firm clean electricity that can operate continuously, as opposed to intermittent sources like solar and wind. Major hyperscalers including Google, Amazon, and Microsoft have collectively contracted approximately 135 gigawatts of clean power capacity, but intermittent generation alone cannot satisfy their round-the-clock needs.

Battery storage remains economically challenging for long-duration applications. While suitable for short-term buffering, current storage technology cannot cost-effectively replace baseload generation for facilities requiring continuous multi-megawatt supply. This gap between corporate climate commitments and technical limitations creates the market opportunity that firms like Fervo are positioned to address.

Geographic and Infrastructure Constraints

Regional power grid limitations significantly affect AI data center placement decisions. Texas, Virginia, and parts of the Western United States have experienced concentrated data center growth, but grid interconnection delays now stretch to seven years in some regions. This creates a bottleneck where computational demand outpaces the power infrastructure required to support it.

Industry analysts suggest that AI could emerge as one of the largest new electricity demand drivers in decades, reshaping energy market considerations around reliability and capacity. U.S. electricity load is expected to grow by as much as 50% by 2035, driven substantially by AI workloads. These constraints create investment opportunities in alternative energy sources that can deliver power where and when tech companies need it.

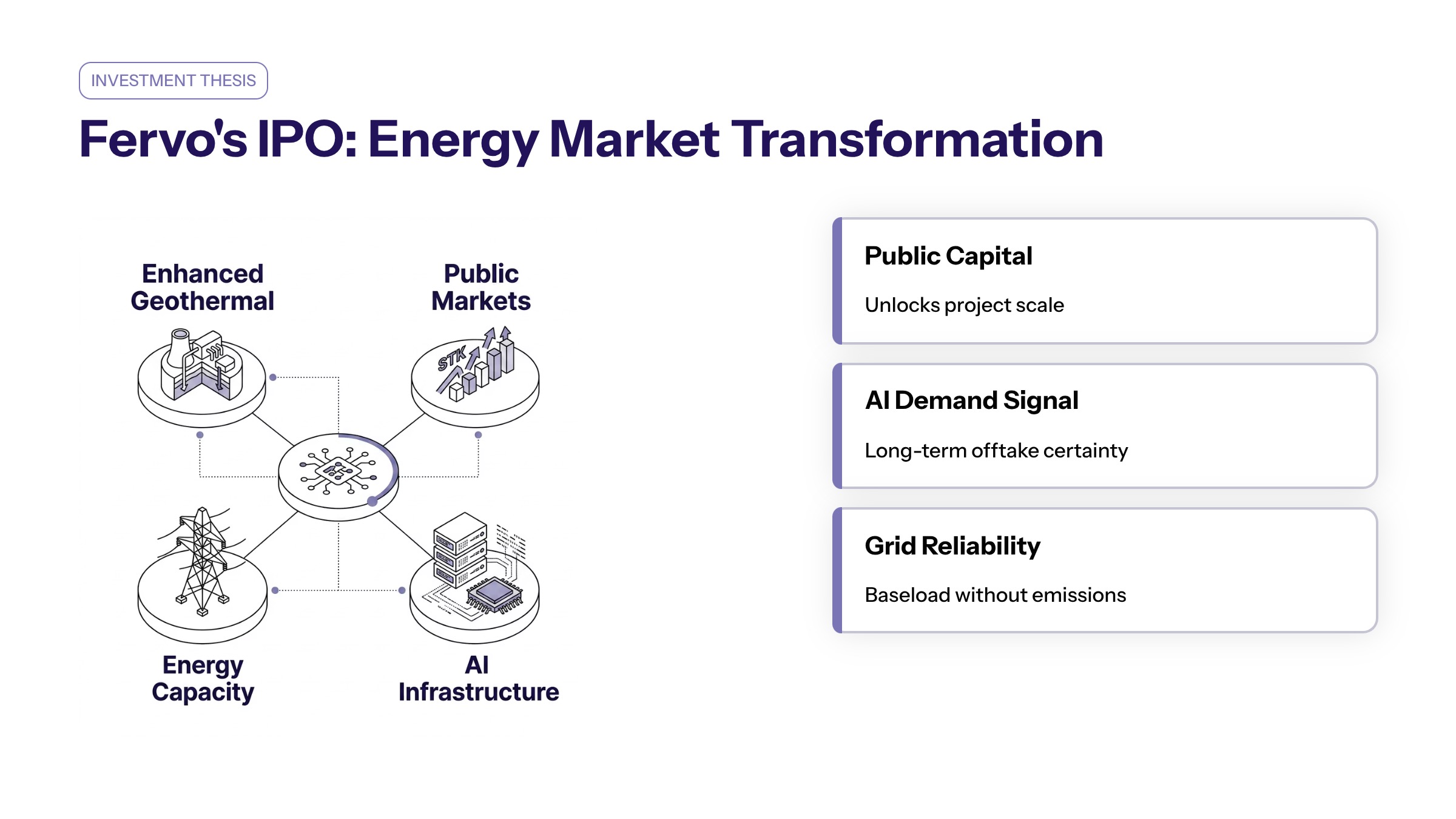

How Fervo’s IPO Reflects the Energy Market Transformation

Fervo’s IPO is part of a broader investment surge into advanced energy technologies. The timing reflects investor recognition that electricity demand from AI infrastructure requires new generation capacity that traditional renewable sources cannot provide alone.

Market Timing and Investor Confidence

The company’s valuation of up to $7.37 billion reflects strong investor optimism but also sets a high bar for future performance. This premium valuation signals that investors view scarcity of reliable, always-on clean power as central to future energy infrastructure value. Fervo’s revenue trajectory supports this confidence: 2025 revenue reached approximately $90 million, with 2026 guidance between $300 million and $400 million.

Fervo’s IPO reflects a shift in energy market investments, moving from a focus on solar and wind to technologies that can provide reliable, round-the-clock electricity, such as geothermal and nuclear power. Underwriting by major financial institutions including Morgan Stanley, Bank of America, Barclays, and RBC Capital demonstrates institutional confidence in both the technology and market demand projections.

Strategic Partnerships with Tech Giants

Google represents approximately 65-70% of Fervo’s contracted revenue through 2028, providing visibility that supports the company’s valuation. The financial viability of energy companies hinges on agreements with major tech firms to fulfill their clean energy requirements. Google has committed to approximately 115 megawatts of geothermal capacity from Fervo specifically for its data center operations.

Companies are moving from simply consuming electricity to investing directly in new energy generation to guarantee clean power supply. These corporate power purchase agreements provide the revenue certainty that enables capital-intensive infrastructure development. Other hyperscalers including AWS and Microsoft are in earlier-stage commitments, suggesting expansion potential beyond current contracted capacity.

From Niche to Mainstream Energy Infrastructure

The geothermal market, currently providing less than 1% of global electricity generation, is expected to grow significantly, with advanced geothermal systems potentially producing over 90 gigawatts of electricity in the U.S. under favorable conditions. This represents a transformation from traditional geothermal development, which was limited to areas with existing hydrothermal resources.

Advanced Enhanced Geothermal Systems (EGS) utilize drilling techniques adapted from the oil and gas sector to supply scalable geothermal energy. This technology transfer enables development in locations previously considered unsuitable for geothermal power generation, dramatically expanding the total addressable market for the industry.

Enhanced Geothermal Technology and Market Implementation

Fervo’s approach addresses both AI power needs and climate change goals by delivering carbon-free baseload electricity. The company’s technology development demonstrates how innovation can expand geothermal capacity beyond traditional limits.

Enhanced Geothermal Systems (EGS) Technology

Enhanced geothermal systems (EGS) utilize horizontal drilling and hydraulic fracturing techniques to access underground heat in a wider range of locations, potentially expanding geothermal development significantly. Unlike conventional geothermal, which requires naturally occurring hydrothermal reservoirs, EGS creates permeability in subsurface rock to circulate water and extract heat.

Fervo has integrated AI-powered drilling optimization that has reduced well completion times dramatically. In Utah, one ultra-deep well was drilled in 16 days compared to previous durations of months. This efficiency improvement reduced costs from approximately $9.4 million per well to $4.8 million. Cape Station, Fervo’s flagship project, targets initial generation of approximately 100 megawatts, expanding toward 400 megawatts by 2027.

Project Red demonstrated the viability of Fervo’s approach, producing 3.5 megawatts of baseload power with flow rates of 60 liters per second. Field results show power capacity density in certain reservoirs of 9.1 megawatts per cubic kilometer—approximately 5-10 times the density of conventional hydrothermal systems.

Cost Reduction and Competitive Positioning

Installed cost for Cape Station currently stands at approximately $7,000 per kilowatt. Fervo expects to reduce this to $3,000 per kilowatt to achieve cost competitiveness with natural gas generation. Drilling costs represent the single largest expense in geothermal development, accounting for 30% to 57% of plant development costs, making cost reduction a critical factor for competition in the sector.

Recent data indicates a 12% to 26% decline in drilling costs for vertical wells, which could transform the feasibility of enhanced geothermal systems and broaden geographic deployment. Each megawatt of EGS capacity requires approximately $5-7 million upfront, creating substantial capital requirements but also establishing barriers to entry that benefit established developers.

Revenue Model and Project Pipeline

Fervo’s development portfolio spans multiple stages, from operational capacity to early-stage opportunities:

|

Development Stage |

Capacity |

Status |

|---|---|---|

|

Operational |

3 MW |

Delivering electricity |

|

Under Construction |

~100 MW |

Cape Station Phase 1 |

|

Advanced Development |

~400 MW |

Cape Station expansion |

|

Early-Stage Review |

40+ GW |

Pipeline opportunities |

The company’s $7.2 billion revenue backlog represents contracted future revenue from power purchase agreements. Fervo’s capital expenditures are projected to be approximately $1.2 billion for the year, with significant funding needed for the second phase of its Cape Station project, which is mostly unfunded. The IPO raise directly addresses this funding gap.

Market Challenges and Implementation Solutions

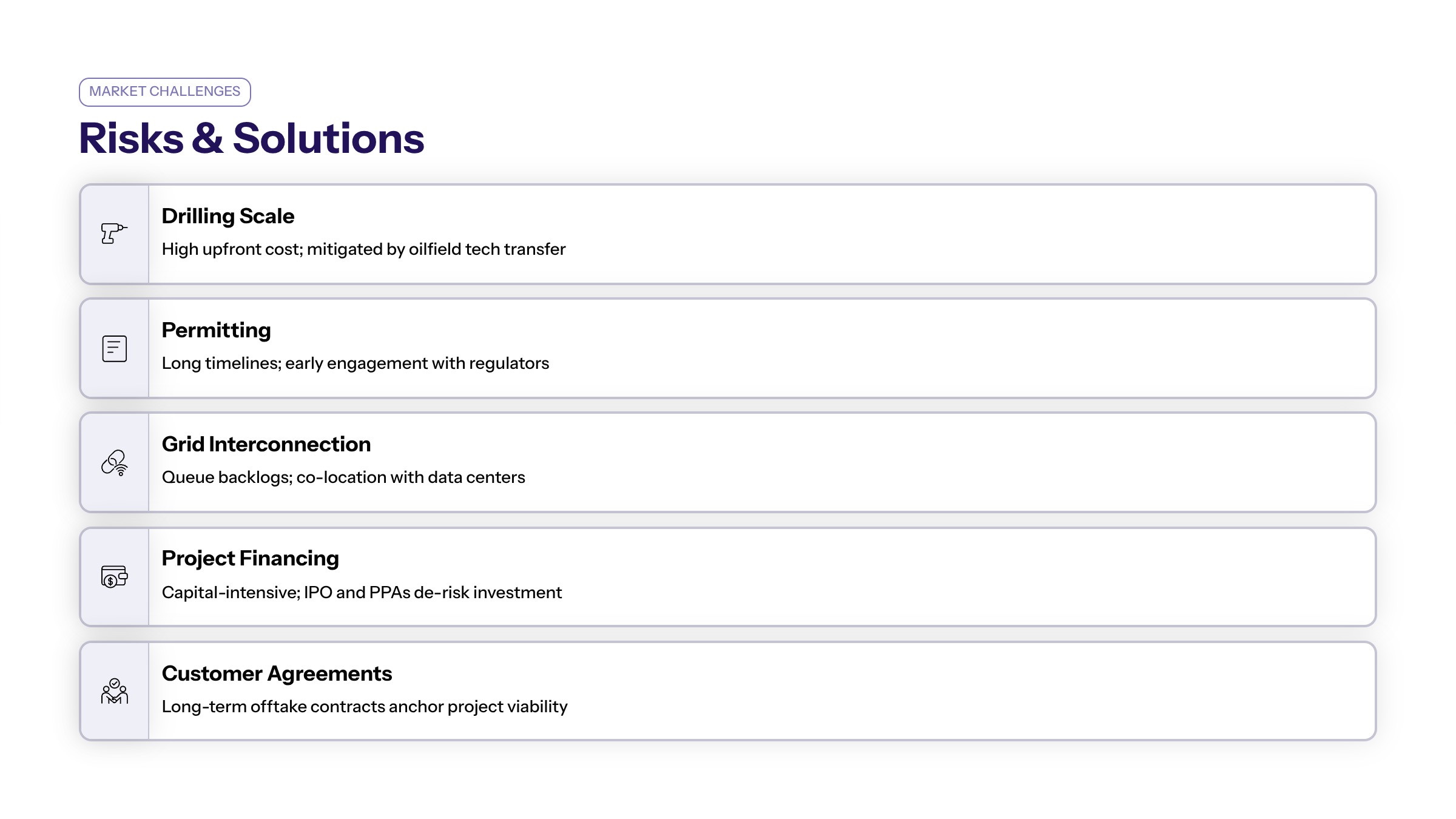

Despite strong market fundamentals, Fervo faces execution risks that investors and partners must evaluate. Understanding these challenges provides context for assessing the company’s path to profitability.

High Capital Requirements and Extended Development Timelines

The company faces execution risks related to managing capital intensity and project timelines, as drilling costs account for 30% to 57% of plant development costs, which can be affected by unforeseen technical issues. Fervo is not GAAP-profitable yet, with profitability projected for 2028-2029 assuming successful revenue growth and cost management.

IPO proceeds will fund project development, land acquisition, and operational scaling. The increased energy demands from AI data centers necessitate faster deployment of new energy technologies, creating pressure to accelerate development while managing construction and drilling risks.

Regulatory and Policy Dependencies

Federal support influences both development timelines and investor risk perception. The Next-Generation Geothermal Research and Development Act provides legislative backing for EGS technology advancement. The U.S. Department of Energy estimates that enhanced geothermal systems could produce over 90 gigawatts of electricity in the U.S. under optimal conditions, representing a substantial increase from current geothermal capacity.

State-level regulatory frameworks in Texas, Colorado, and other key regions affect permitting timelines and operational requirements. Streamlining environmental reviews and water rights processes could accelerate deployment, while regulatory delays would extend development periods and increase costs.

Technology Scaling and Cost Competitiveness

As of 2024, two operators, Ormat and Calpine, account for 69% of installed geothermal capacity and a similar share of operating plants in the U.S., indicating a concentrated market dominated by established players. Fervo’s ability to scale operations while maintaining drilling success rates will determine whether it can achieve lower costs and competitive positioning.

The geothermal market is currently small compared to solar and wind energy, providing less than 1% of global electricity generation, but advanced geothermal systems could significantly expand this capacity. Grid integration remains challenging—transmission build-out lags demand growth, and interconnection delays can strand otherwise viable projects.

The demand for clean, continuous energy to support AI operations is significantly influencing capital flows toward infrastructure projects focused on energy generation. This capital availability supports development but also creates competition for skilled workers, equipment, and grid access.

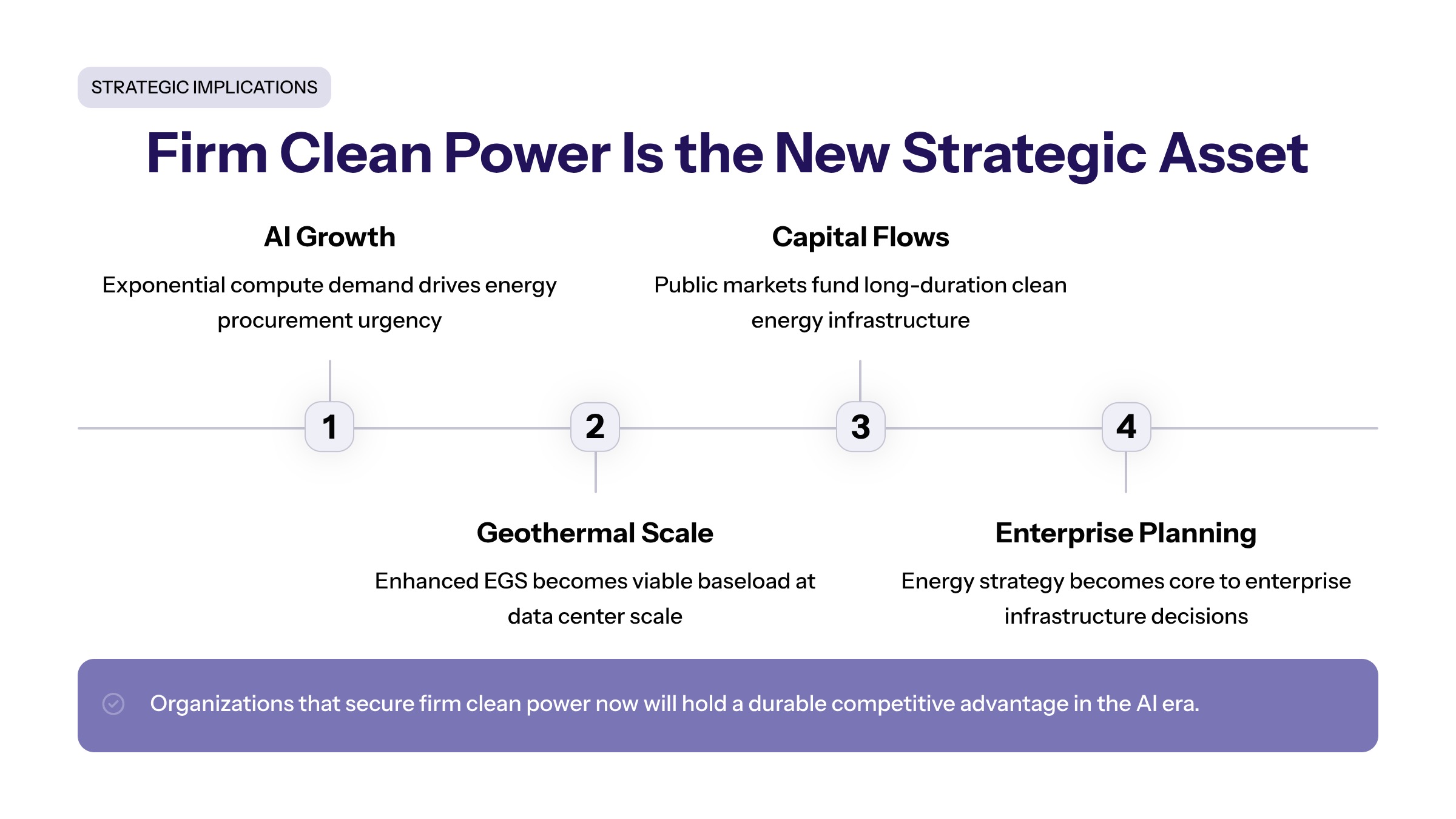

Conclusion and Strategic Implications

Fervo Energy’s IPO validates the intersection of AI growth and clean energy infrastructure needs. The $1.33 billion raise under the FRVO ticker demonstrates that investors recognize AI data centers are reshaping U.S. energy demand in ways that create durable market opportunities for firm clean power providers.

For enterprise technology leaders, the implications are immediate:

-

Evaluate power procurement strategies that include geothermal and other firm renewable sources alongside solar and wind

-

Assess data center location decisions based on grid reliability and clean power availability

-

Consider direct investment or long-term power purchase agreements with EGS developers to secure supply

Organizations planning computational infrastructure expansion should factor energy constraints into capacity planning. AI data centers are driving a significant increase in electricity demand, with projections indicating that electricity use by data centers could spike by 2030 due to the growing adoption of AI technologies worldwide.

Related considerations include grid reliability planning, carbon accounting frameworks that value 24/7 clean electricity, and long-term energy cost management in an environment where new natural gas plant costs have surged approximately 66% in two years. The transformation Fervo’s IPO represents will continue reshaping how organizations think about the relationship between computational capacity and energy infrastructure.

Additional Resources

For technical specifications on enhanced geothermal systems and regulatory frameworks, the U.S. Department of Energy’s geothermal technologies office provides comprehensive documentation on EGS development standards and permitting requirements.

Corporate renewable energy procurement guidance is available through industry organizations focused on power purchase agreement structures and carbon accounting methodologies. These resources help organizations navigate the shift from simple electricity consumption to strategic energy partnership development.

AI infrastructure planning resources addressing energy-conscious development strategies continue to evolve as the market matures. Enterprise technology teams should establish ongoing monitoring of geothermal project development, grid capacity expansion, and regulatory changes affecting firm clean power availability in target regions.