Samsung Strike Talks Expose AI Memory Chip Supply Chain Risk

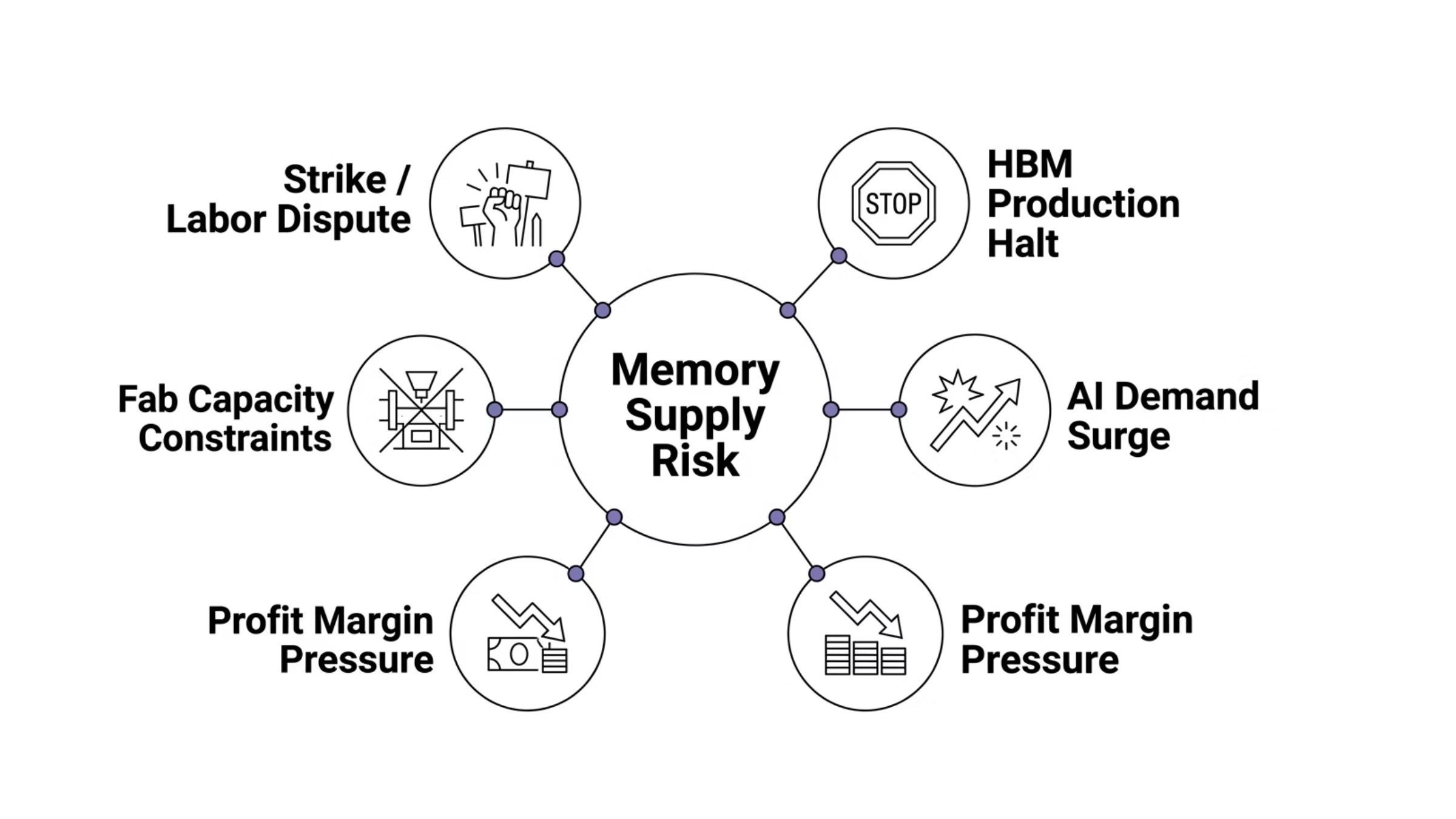

Samsung AI chip strike risk is now a direct supply-chain issue for enterprises because Samsung Electronics is negotiating under the threat of an 18-day walkout by more than 45,000 workers in the memory division that supplies DRAM, NAND, and high bandwidth memory for AI systems. If the Samsung strike proceeds, the disruption could tighten an already constrained memory market, raise memory prices, delay AI hardware deliveries, and weaken customer confidence in chip shipments.

This article covers the strike timeline, the union’s demands, affected production assets, likely pricing effects, and practical planning steps for IT leaders, supply chain managers, AI infrastructure teams, and enterprise procurement groups. The focus is not general labor politics; the focus is how Samsung’s memory chip workers, Samsung’s memory chip plants, and South Korea’s semiconductor concentration affect the AI chip supply chain.

The direct answer: Samsung’s labor dispute threatens HBM memory and DRAM production that are critical for AI infrastructure, GPU servers, AI data centres, and devices that run AI applications. Because strong AI demand has already absorbed available high-end capacity, even a short supply disruption can create a wider supply shock across the global technology industry.

You will come away with a clearer view of:

The Samsung strike timeline and why unlike past labor disputes, this conflict matters to AI supply chain stability.

The compensation dispute behind the walkout threat, including operating profit sharing and performance bonuses.

The memory chips most exposed, including HBM4, enterprise DRAM, and NAND flash.

The likely impact on memory prices, delivery timelines, and AI hardware risk.

Practical business continuity steps for reducing dependency on fragile global supply chains.

Understanding the Samsung Labor Crisis

The current strike talks involve Samsung Electronics workers in the Device Solutions division, the business unit that includes Samsung’s memory division and semiconductor operations. The National Samsung Electronics Union (NSEU) represents more than 45,000 workers, and Samsung’s unionized workers plan an 18-day strike beginning May 21, 2026, if last-ditch talks fail. Samsung management and union leaders are in emergency talks following the failure of initial government-mediated discussions, including processes associated with the national labor relations commission.

Samsung’s unions are demanding that 15% of operating profit be allocated to a bonus pool, the removal of the current cap on bonuses, and a 7% wage hike, reflecting the growing discontent among workers regarding compensation. The union’s demands are tied to the AI boom: Samsung’s memory chip workers argue that annual operating profit directly generated by memory chips should be shared more structurally, not only through one-time payments.

Samsung’s proposed bonus structure for its memory chip employees could reach 607% of their annual salary, while employees in the logic chip and foundry divisions may receive bonuses between 50% and 100% of their annual salary, highlighting a significant disparity in compensation within the company. That internal gap matters because Samsung’s memory business is benefiting from the global AI boom, while the logic chip market, foundry operations, and other logic chip businesses face different economics.

The legal and policy environment may also shape the outcome. The South Korean Prime Minister may invoke emergency arbitration rights to halt the strike and enforce a cooling-off period. A South Korean court granted an injunction ordering that safety and anti-deterioration teams remain staffed during the potential strike. A South Korean court has also ruled that the union cannot legally disrupt or obstruct physical fabrication operations, with fines of 100 million won per day for violations.

Financial Stakes Behind the Dispute

The financial stakes are unusually high because Samsung’s operating profit increased nearly eightfold in Q1 2026, highlighting its recovery and competitiveness in the memory chip market after a downturn. Samsung’s record Q1 2026 results followed a weak memory downturn in which Samsung paid zero or very limited bonuses to many memory workers in 2024. The expectation gap is simple: workers absorbed the downside of the memory cycle and now want a larger share of the upside created by the AI era.

Samsung’s labor dispute highlights the growing tension in the tech industry regarding fair compensation, as workers demand a larger share of profits generated from the AI boom, which has disproportionately benefited certain divisions over others. Samsung’s memory division produces the DRAM, NAND, and HBM memory that now sits at the center of AI infrastructure, while logic chips and foundry work have not captured the same near-term pricing power.

Competitive pressure from SK Hynix has intensified the dispute. SK Hynix has removed its long-term pay cap and increased bonuses, which has led to dissatisfaction among Samsung employees, resulting in approximately 200 workers leaving Samsung for SK Hynix in just four months. SK Hynix’s bonus model is tied to roughly 10% of operating profit, and projected worker payouts have been discussed at levels that could approach $900,000 next year, depending on profitability.

The dispute also intersects with market sentiment in South Korea. Government officials and investors are watching whether labor instability will affect customer trust, capital flows, and South Korea’s economic position. Korean retail investors flooded into semiconductor-related trades during the AI industrial boom, and Samsung’s role in the index’s total market cap makes the outcome financially visible beyond the chip industry. Separate political debates, such as Kim’s citizen dividend comments, Kim’s personal opinion on redistributing excess tax revenue, or any corporate tax bill, should not be confused with the immediate operational risk inside Samsung’s semiconductor division.

Production Assets at Risk

The exposed assets include Samsung’s memory chip plants in Pyeongtaek, Hwaseong, and Giheung, with Hwaseong and Giheung especially important for DRAM and NAND flash production. These facilities support Samsung’s memory chip output across enterprise servers, mobile devices, SSDs, cloud infrastructure, and AI systems.

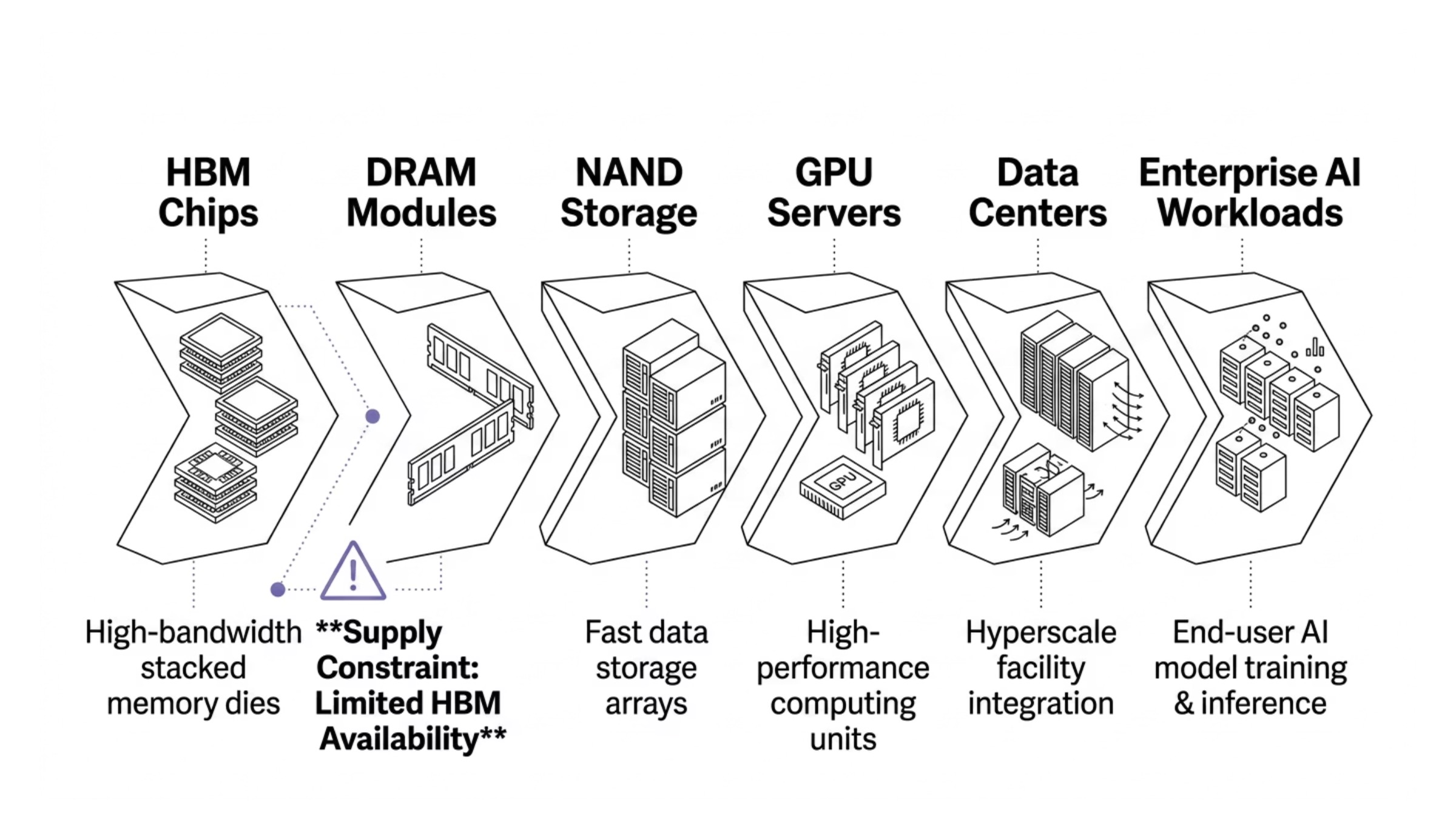

The most strategically important lines are HBM4 manufacturing lines. High bandwidth memory is built from memory chips stacked alongside GPUs or accelerators, providing the bandwidth and energy efficiency required by AI chips used in training and inference. HBM4 is especially important because AI data centres are scaling clusters around accelerator platforms where memory bandwidth determines real-world throughput.

Samsung has begun scaling back wafer inputs in anticipation of the strike, implementing emergency “warm-down” procedures to minimize material loss. Samsung reportedly planned to shift production mix toward higher-value products, including HBM and server DRAM, while reducing exposure to wafer scrap. Halting semiconductor fabrication lines mid-process results in scrapping delicate silicon wafers, costing roughly $20,000 per wafer, so chip fabrication mid process cannot be stopped like an assembly line.

This is why labor tension becomes supply chain vulnerability. Even if courts require safety staffing and prevent physical obstruction, advanced fabs depend on skilled engineers, process oversight, maintenance, quality checks, and yield control. Samsung believes memory shortages driven by AI demand could last into 2027, and a labor shock would arrive at exactly the wrong point in the cycle.

AI Memory Chip Supply Chain Exposure

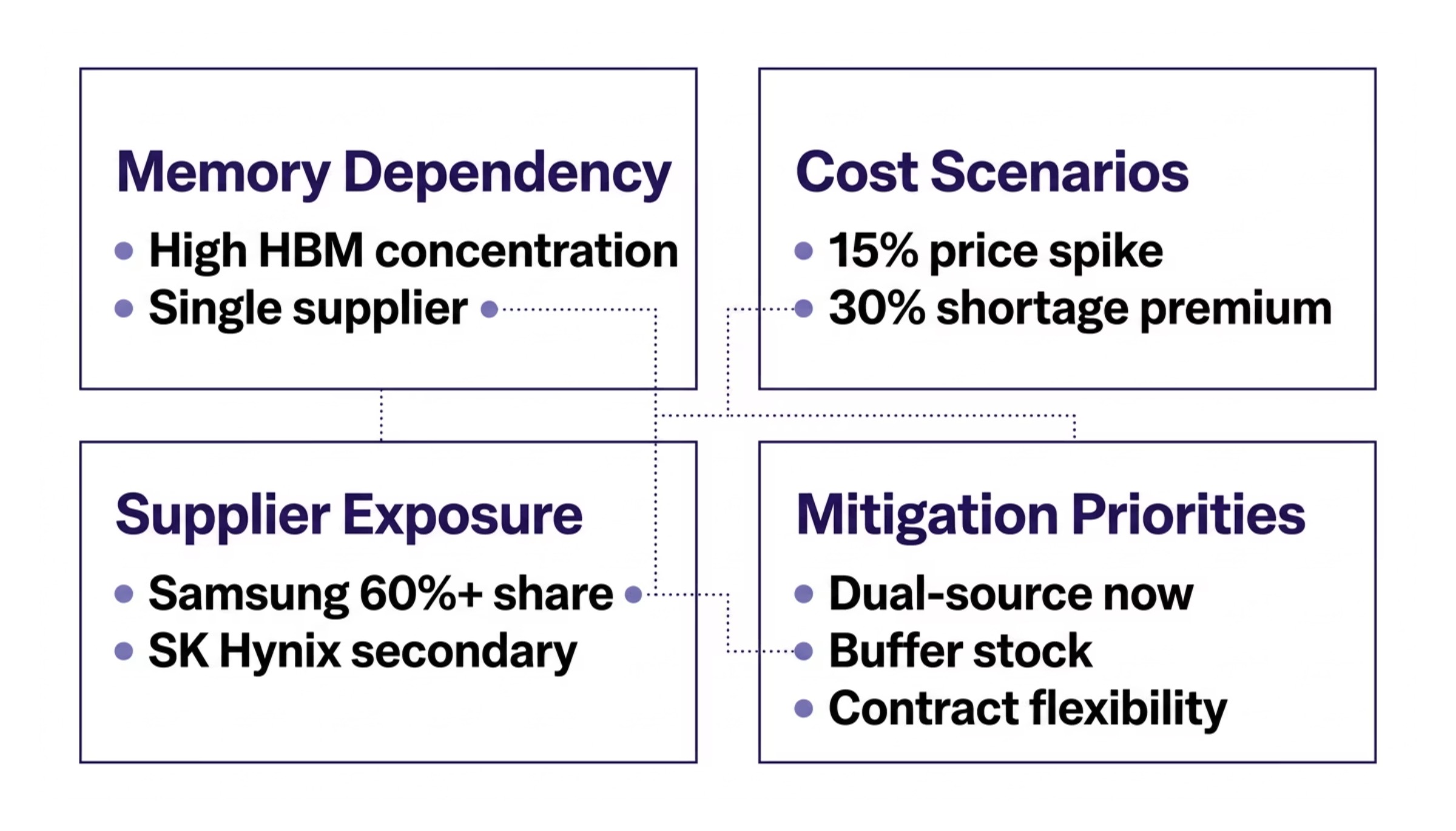

Samsung holds a commanding share of the global memory chip market, making Samsung Electronics a critical player in the semiconductor industry, especially in the context of AI demand. Samsung has long held a DRAM market share lead, with roughly about a third or more of the global DRAM market depending on the reporting period, and Samsung has historically been viewed as the world’s largest DRAM maker.

That position is changing under AI pressure. The competitive landscape in the memory chip market is shifting, with Samsung’s recent struggles allowing SK Hynix to overtake it as the world’s largest DRAM maker for the first time in 33 years. Samsung’s competitors, SK Hynix and Micron, have been gaining market share in high-bandwidth memory, with SK Hynix capturing 62% of the global HBM market as Samsung’s share fell to 17%.

Samsung’s HBM3E products previously struggled to pass Nvidia’s qualification standards, while SK Hynix secured premium global contracts. Samsung reclaimed some momentum with HBM4, and HBM4 reportedly outperformed early expectations after launch, but any prolonged Samsung strike could disrupt that recovery.

Critical Memory Components Under Threat

The most important components under threat are HBM4 chips used in NVIDIA AI accelerators, AI training clusters, and data center servers. HBM memory places memory chips stacked alongside advanced processors, enabling high throughput over short physical distances. In practical terms, HBM limits or unlocks how efficiently AI chips can train large models and serve inference workloads.

Enterprise-grade DRAM is also exposed. Cloud providers, hyperscalers, telecom operators, and edge computing platforms use DRAM across servers, storage controllers, networking gear, and AI infrastructure. If Samsung’s memory chip output falls, enterprise-grade DRAM allocation can tighten even for customers not directly buying HBM.

NAND flash storage faces indirect pressure. NAND is essential for AI training datasets, model deployment, SSD-based storage, and enterprise hardware refreshes. An 18-day stoppage at Samsung is expected to create severe supply vacuum, driving significant price hikes across DRAM and NAND flash memory.

The risk extends beyond advanced memory. Expanding legacy memory production is not a quick fix, because legacy memory production still requires qualified capacity, equipment, clean-room scheduling, and skilled labor. Spot prices for DDR4 memory have jumped 20% due to anticipatory stockpiling in the face of potential production shortfalls, and monitoring of DDR4 spot prices in China revealed a spike of 20% due to anticipation of the strike, impacting memory market pricing.

Customer Impact Scenarios

A potential 18-day strike at Samsung could significantly reduce memory chip output, affecting AI training clusters and devices that run AI applications, which may lead to increased memory prices due to tight market conditions. The production halt would affect Q2 chip deliveries first, but the restart window could extend the disruption if yield stabilization takes additional time.

An 18-day strike at Samsung could create a supply shock in the global AI hardware ecosystem, delaying GPU shipments and pushing up server costs due to Samsung’s commanding share of the memory chip market. Production losses from an 18-day strike at Samsung are estimated between 30 trillion and 100 trillion won, depending on assumptions about affected lines, wafer losses, delayed output, and customer penalties.

If Samsung’s strike leads to a significant reduction in memory chip output, it could tighten an already constrained market and put upward pressure on memory prices, as demand from AI data centers continues to rise. Analysts forecast standard DRAM prices to climb 47% to 125% during 2026 because of high bandwidth memory reallocation. That means customers may face price increases even when they are buying standard DRAM rather than HBM.

Large customers are already behaving as if supply risk is real. Apple held emergency meetings with Samsung’s semiconductor division to secure supply for future devices, and reports that Apple accepted immediately available commitments show how fast major OEMs can move when memory availability becomes uncertain. For enterprise buyers, the same pattern means faster contracting, more prepayments, and less room to rely on spot markets.

Competitive Landscape Shifts

SK Hynix is positioned to capture market share during Samsung disruptions because SK Hynix already holds a stronger position in the global HBM market and has reduced labor friction through a structural bonus model. Prolonged labor instability may lead hyperscale data center operators to shift orders to rival companies like SK Hynix or Micron for stability.

Micron, the American semiconductor company Micron, can benefit from diversification demand, but Micron and other suppliers have capacity limitations for enterprise customers. Memory production cannot be added quickly, especially in HBM, where stacked dies, advanced packaging, thermal management, and qualification cycles constrain supply.

The geographic concentration risk is also significant. South Korea remains central to global memory chip market capacity, and supply chain stability in South Korea affects global supply chains for AI infrastructure. The potential strike at Samsung has raised concerns among government officials and investors about its impact on customer trust, capital flows, and South Korea’s economic position, highlighting the interconnectedness of labor relations and supply chain stability in the semiconductor industry.

For Samsung chairman Jay Y. Lee and Samsung management, the strategic issue is larger than one compensation negotiation. The Samsung strike could have broader implications for labor relations in advanced manufacturing, as it raises questions about how companies balance short-term profitability with long-term strategic investments in talent retention and compensation.

Enterprise Risk Assessment and Mitigation

Enterprise risk assessment should treat the Samsung strike threatens AI memory chip supply chains scenario as a business continuity event, not only a procurement issue. AI infrastructure depends on memory chips, GPUs, servers, networking equipment, storage, and deployment timelines that are tightly linked. A disruption in one memory component can delay an entire rack, cluster, or data center buildout.

The ongoing labor dispute could increase budget pressures on the AI economy by driving up infrastructure deployment costs due to high memory prices. If Samsung’s memory chip output falls while AI demand continues to rise, enterprises may pay more for servers, wait longer for hardware, and delay revenue-generating AI workloads.

Cognativ’s view is that enterprises should model this as a physical supply-chain constraint inside the AI boom. Software roadmaps, model deployment schedules, and modernization programs increasingly depend on hardware availability. A practical assessment should connect supplier risk, inventory buffers, architecture choices, and financial exposure.

Supply Chain Vulnerability Analysis

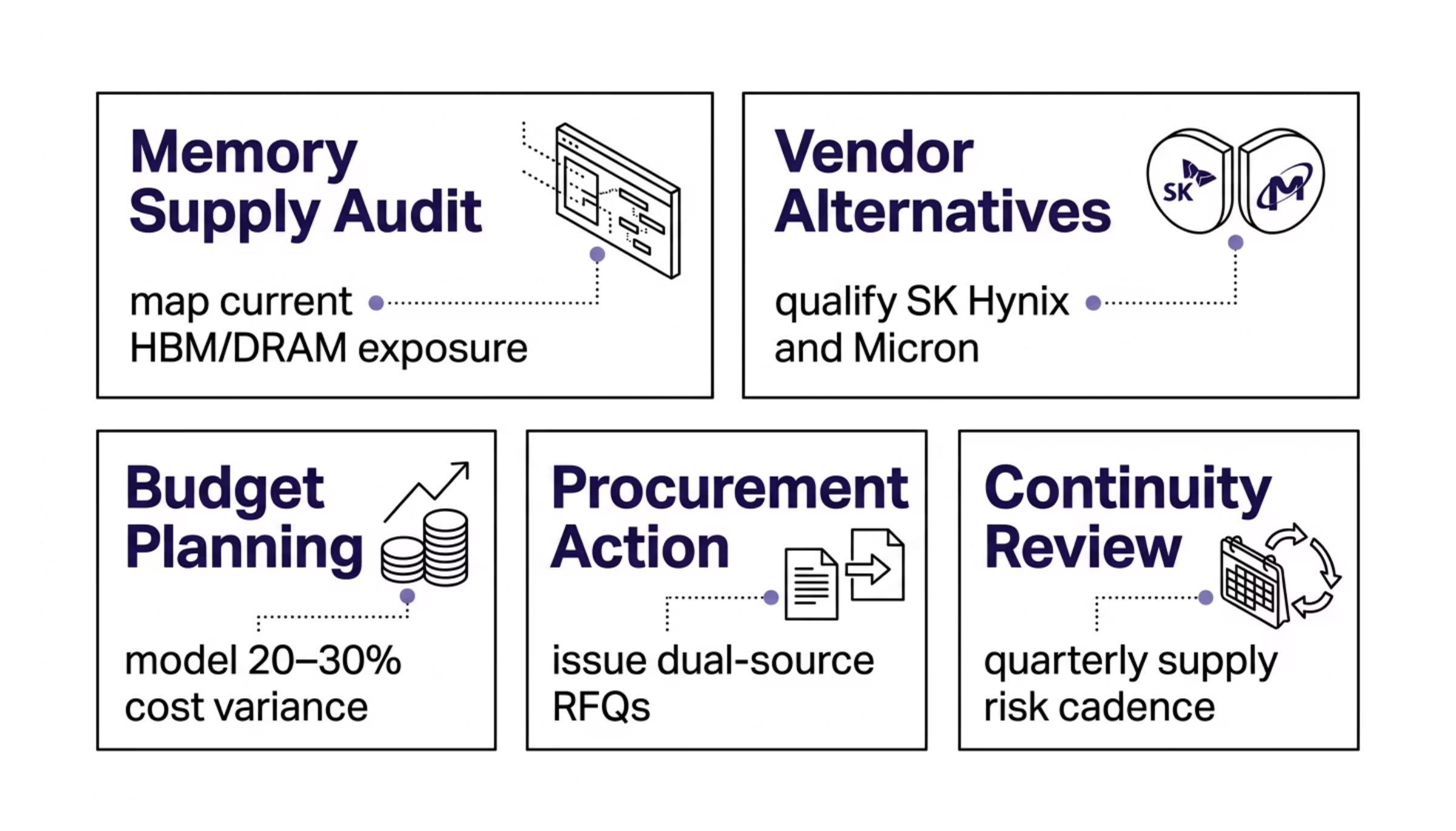

Start by mapping memory chip dependencies across AI infrastructure and enterprise systems. Identify which servers use HBM memory through GPU accelerators, which systems rely on DDR5 or DDR4 DRAM, and which storage platforms depend on NAND flash. Include AI training clusters, inference platforms, edge devices, cloud commitments, and hardware refresh cycles.

Next, identify single-source supplier risks in current procurement strategies. If a server platform, OEM agreement, or accelerator configuration depends heavily on Samsung’s memory chip supply, document which alternatives are qualified from SK Hynix, Micron, or regional suppliers. This matters because supply disruption can occur even when Samsung’s fabs remain partially automated and legally protected from obstruction.

Then quantify potential revenue impact from delayed hardware deployments. Delayed GPU shipments can postpone AI product launches, customer pilots, internal automation projects, and model training schedules. If a six-week disruption window pushes infrastructure into the next quarter, finance teams should model deferred revenue, higher operating costs, and possible contract penalties.

Finally, evaluate inventory buffers and supplier relationship diversification needs. Enterprises dependent on AI systems should assess whether they have enough HBM, DRAM, NAND-backed SSDs, or completed server inventory to bridge a disruption. The right answer differs by workload criticality, but a 90-to-120-day planning horizon is more realistic than just-in-time procurement during a memory chip shortage.

Financial Impact Projections

Memory price increases of 20% to 40% are plausible during near-term supply constraints, especially for AI-grade memory and enterprise server configurations. The risk is not limited to HBM4. When fabs prioritize high-margin HBM memory, standard DRAM and NAND can tighten because capacity is reallocated away from commodity output.

Analysts forecast standard DRAM prices to climb 47% to 125% during 2026 because of high bandwidth memory reallocation, showing how AI demand can inflate costs across the broader memory market. Spot prices for DDR4 memory have already jumped 20% due to anticipatory stockpiling, and DDR4 spot prices in China spiked 20% on strike anticipation. Those moves show that procurement teams are not waiting for a full stoppage before repricing risk.

Extended delivery timelines are also likely for AI servers and enterprise hardware refresh cycles. An 18-day stoppage can create a longer recovery period if wafer scrap, process recalibration, quality inspection, and customer requalification slow the restart. Halting fabrication mid-process can destroy wafers worth roughly $20,000 each, so production economics can amplify physical delays.

Budget teams should plan for alternative supplier relationships, expedited logistics, prepayment requirements, and contract renegotiation. Combined operating profit across Samsung’s memory and semiconductor operations explains why workers are pressing for higher performance bonuses, but the same operating profit pool also signals how much enterprise demand depends on stable output.

Common Supply Chain Challenges and Solutions

Semiconductor disruptions reward companies that plan before shortages become visible in delivery schedules. The Samsung AI chip strike risk is a reminder that supply chain resilience now includes labor relations, qualification standards, capacity allocation, geopolitical exposure, and supplier compensation models.

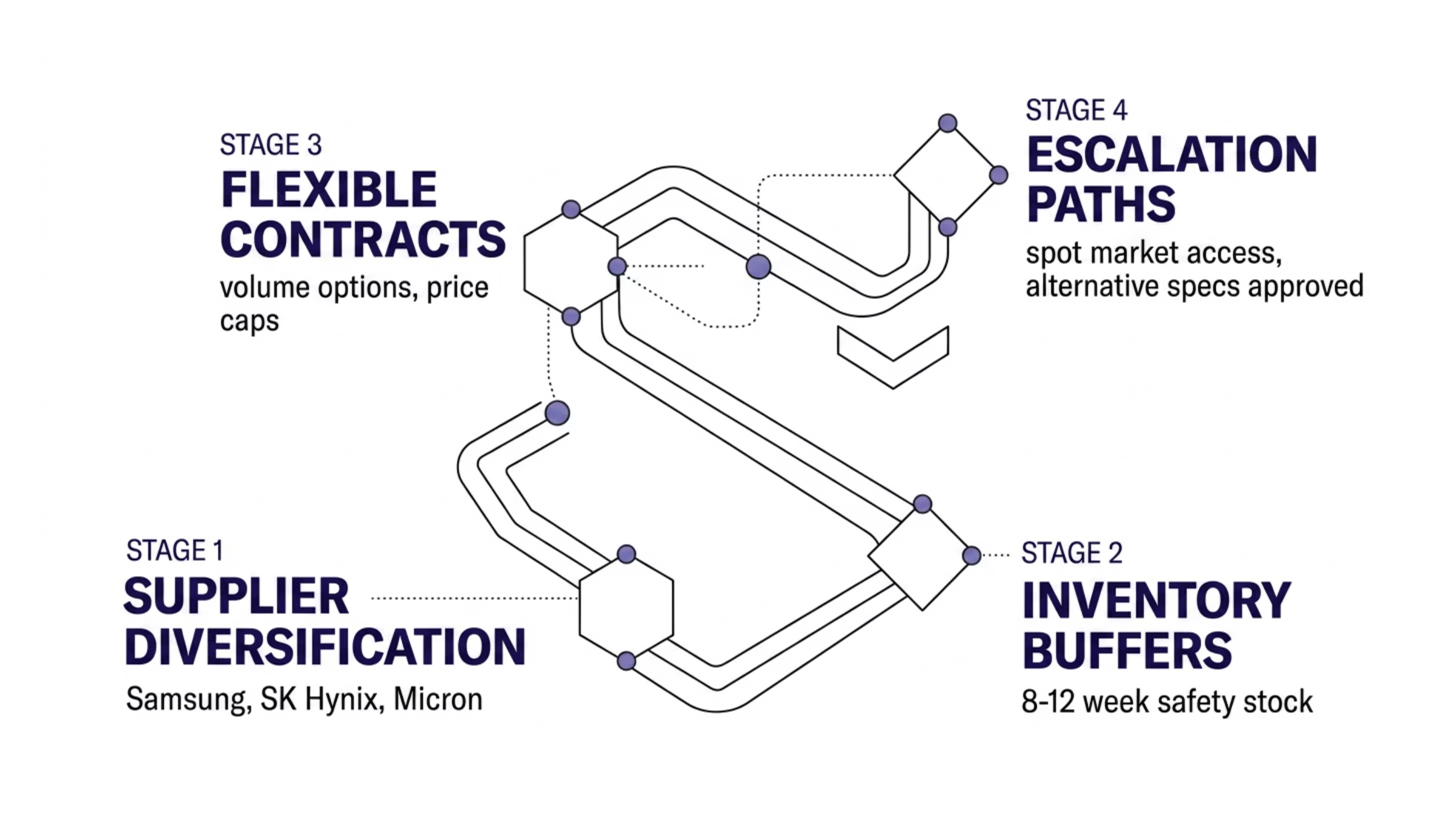

Limited Supplier Diversification

The challenge is overreliance on Samsung’s memory chip supply in AI infrastructure, cloud hardware, or device roadmaps. Establish qualified vendor relationships with SK Hynix, Micron, and regional suppliers before crises emerge.

The practical solution is to create a dual-source or multi-source roadmap for HBM memory, enterprise DRAM, and NAND flash. Qualification should include technical performance, firmware compatibility, warranty terms, delivery history, and the supplier’s labor stability. Hyperscale data center operators may shift orders to SK Hynix or Micron for stability if prolonged labor instability continues, but enterprises without prequalified suppliers will have less leverage.

Inadequate Inventory Planning

The challenge is assuming just-in-time delivery will work during a memory chip shortage. Implement strategic stockpiling for critical memory components with 90-to-120-day buffer periods.

This buffer should not be a blanket purchase of every part number. Prioritize HBM-equipped accelerator systems, AI server platforms, SSDs tied to model deployment, and replacement memory for critical enterprise systems. If memory prices rise quickly, strategic inventory can protect deployment schedules and reduce emergency spot-market buying.

Reactive Procurement Strategies

The challenge is waiting until force majeure conditions, allocation notices, or price spikes appear before changing contract terms. Develop flexible contracting terms allowing supplier substitution during force majeure events.

Contracts should include supply disruption clauses, price-adjustment guardrails, alternate part approval workflows, and escalation paths with OEMs. Procurement should also monitor court decisions, emergency arbitration risk, and Samsung management updates because legal outcomes can change strike timing without eliminating longer-term labor pressure.

Conclusion and Next Steps

Samsung’s labor dispute matters because the AI boom depends on physical supply chains that can break through labor, capacity, quality, and concentration risk. Samsung Electronics remains a critical force in memory chips, and any major supply disruption in Samsung’s memory division can affect AI chips, GPU shipments, AI data centres, enterprise servers, and devices that run AI applications.

Immediate next steps for enterprise teams:

Audit memory chip dependencies across AI infrastructure, server refreshes, storage platforms, and edge systems.

Identify where Samsung is a single-source or dominant-source supplier in current procurement plans.

Evaluate qualified alternatives from SK Hynix, Micron, and regional suppliers.

Build 90-to-120-day inventory buffers for critical HBM, DRAM, NAND, and completed AI server systems.

Update contracts with force majeure language, supplier substitution rights, and price volatility protections.

Model the financial impact of 20% to 40% memory price increases, longer lead times, and delayed AI deployments.

Related considerations include semiconductor geopolitical risk, alternative memory technologies, advanced packaging capacity, and supply chain resilience planning. For Cognativ clients, the strategic takeaway is clear: AI modernization should include infrastructure risk assessment, cross-supplier architecture, inventory planning, and supplier resilience as part of a practical AI readiness framework.

Additional Resources

Enterprise procurement teams should maintain a short set of working tools for memory market monitoring and supplier comparison:

Memory dependency map: Link each AI workload, server platform, accelerator type, and storage tier to the memory chips required.

Supplier risk scorecard: Compare Samsung Electronics, SK Hynix, Micron, and regional suppliers by capacity, qualification status, labor stability, geography, and delivery performance.

Pricing watchlist: Track HBM memory, DDR5, DDR4, NAND flash, and spot-market movement in China and other major trading hubs.

Contract review checklist: Confirm force majeure coverage, allocation language, supplier substitution rights, and delivery penalty exposure.

AI hardware risk model: Estimate how delayed GPU shipments, server cost increases, and memory prices affect AI infrastructure budgets and deployment timelines.