Semiconductor Volatility Business Risk: Managing AI Hardware Demand in Enterprise Operations

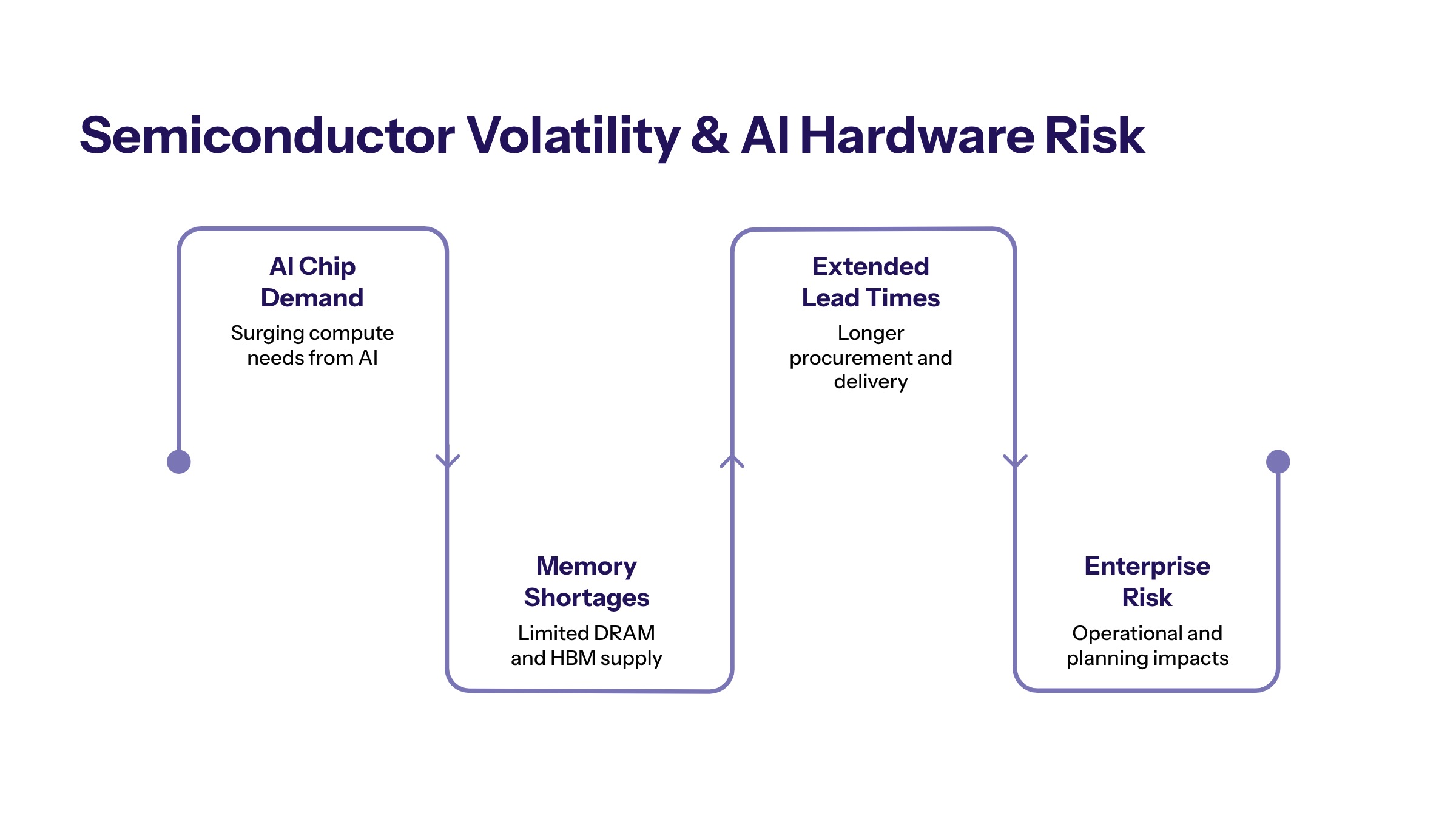

Semiconductor volatility driven by the AI boom has fundamentally reshaped enterprise technology procurement. The demand for AI chips in data centers is projected to consume 70% of memory chips in 2026, leading to long, unpredictable lead times that disrupt traditional planning cycles. For CTOs, procurement leaders, and operations executives, this volatility introduces profound financial, operational, and strategic risks into the artificial intelligence hardware market.

This article covers enterprise risk management for semiconductor dependencies—specifically how organizations can navigate supply constraints, price fluctuations, and extended lead times affecting AI infrastructure projects. We exclude individual investment strategies and stock market speculation, focusing instead on actionable frameworks for technology supply chain management. The content addresses technology leaders responsible for hardware procurement, infrastructure planning, and operational continuity in environments increasingly dependent on AI capabilities.

Direct answer: Semiconductor volatility from AI demand creates 6-12 month delivery delays and 40-80% cost increases for enterprise hardware, requiring proactive supply chain diversification and flexible technology architecture to maintain operational continuity.

By reading this article, you will gain:

Risk assessment frameworks for evaluating semiconductor dependencies across your hardware portfolio

Supply chain diversification strategies to reduce single-supplier vulnerabilities

Technology architecture decisions that balance performance with procurement resilience

Cost management approaches for volatile hardware budgets

Implementation guidance for phased deployment and parallel procurement

Understanding Semiconductor Volatility and Business Risk in AI Hardware Demand

Semiconductor volatility refers to the unpredictable shifts in supply, pricing, and lead times affecting chips, memory, and AI accelerators. In today’s market, this volatility stems from soaring demand for AI infrastructure that far outpaces the industry’s capacity to expand production. The intense demand for advanced high-bandwidth memory (HBM) and GPUs creates severe shortages and drives up component costs in the AI hardware market, fundamentally altering enterprise technology planning assumptions.

For enterprise operations, this volatility affects technology budgeting, infrastructure planning, performance reliability, and supplier relationships. Understanding the underlying dynamics helps organizations anticipate constraints and build more resilient procurement strategies.

Supply and Demand Imbalances Driving Semiconductor Volatility and AI Infrastructure Risks

The AI boom has created a global memory chip shortage, leading to a sharp divide in corporate earnings and stock-market performance, with semiconductor manufacturers benefiting while consumer electronics makers face rising costs. The semiconductor industry is experiencing a shift from consumer electronics manufacturing to high-margin AI data center products due to increasing demand—a structural change that redirects capacity away from traditional enterprise hardware.

Data centers now require 100-500 megawatts of power capacity, creating infrastructure bottlenecks that compound hardware constraints. Advanced packaging methods like CoWoS (Chip on Wafer on Substrate) and cutting-edge fabrication nodes (2-3nm) remain fully allocated, with lead times for 3nm AI logic now exceeding 50 weeks. These supply constraints directly affect enterprise hardware procurement timelines, transforming what were once routine orders into strategic allocation negotiations.

Major suppliers control over 95% of DRAM production, leading to supply chain vulnerabilities. Concentration risk in semiconductor markets, particularly in Taiwan and South Korea, has raised concerns among investors, as these markets are increasingly tied to a few dominant companies like TSMC and Samsung Electronics, which could lead to significant volatility if market sentiment shifts.

Price Volatility Patterns and Impact on Stock Prices Including Western Digital and the P 500

Price volatility for memory chips like DRAM and HBM has doubled in price since early 2025, impacting operating margins for manufacturers. NAND contract prices have climbed more than 600% since late September, while DRAM prices have risen nearly 400%, driven by AI-related demand exceeding available supply. Soaring demand for high-bandwidth memory and AI-related chips has pushed prices sharply higher, benefiting companies like Micron Technology and Samsung Electronics.

The AI expansion has transformed memory chips from a commodity component into a critical supply bottleneck, reshaping the traditional semiconductor cycle and leading to stronger pricing power for suppliers. GPU allocation systems have replaced traditional purchasing for enterprise AI projects—organizations can no longer simply place orders but must secure allocations through volume commitments and long-term contracts.

Server CPU pricing has risen 10-20% since early 2026, reflecting shifting ratios of CPU to GPU in AI workloads. Analysts expect that the memory chip shortage driven by AI demand may persist well into the end of the decade, significantly impacting the semiconductor market dynamics. This pricing volatility directly affects enterprise budget planning and project execution, requiring new approaches to financial forecasting.

Stock market investors have closely watched semiconductor stocks such as Western Digital, which have experienced massive gains amid the AI trade. The P 500 index now includes a significant proportion of AI-related companies, reflecting the sector's growing influence on global equities. Importantly, fluctuations in semiconductor sector fundamentals and implied volatility contribute to broader market risk and underscore the business risk tied to AI hardware demand.

AI Hardware Demand Impact on Business Operations and Stock Market Dynamics

Building on these volatility patterns, enterprises face concrete operational challenges across procurement, cost management, and technology architecture. The transition from predictable hardware cycles to allocation-based systems fundamentally changes how technology teams plan and execute infrastructure projects.

Enterprise Hardware Procurement Challenges Amid Semiconductor Volatility and AI Supply Chain Constraints

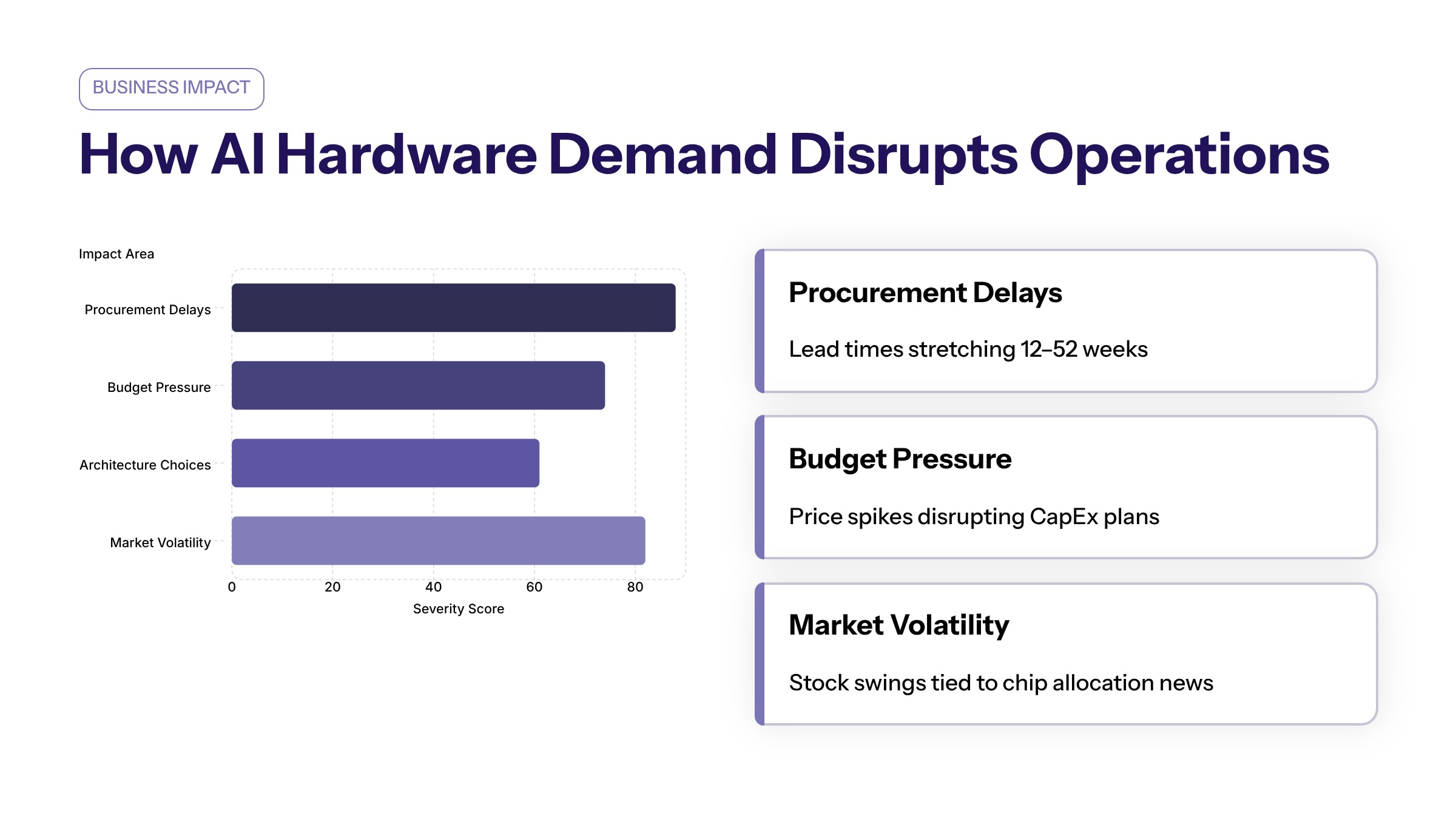

Lead times have extended from traditional 2-4 weeks to 6-12 months for AI-capable servers and accelerators. The scarcity of critical raw materials such as gallium and germanium is contributing to industry volatility, while advanced packaging capacity remains constrained through 2027. Organizations must now forecast hardware needs 12-18 months in advance—a dramatic shift from historical procurement practices.

Allocation-based purchasing has become standard for cutting-edge components. Vendors require NCNR (non-cancellable, non-refundable) orders, advance payments, and volume commitments to secure production slots. The ability of companies to secure long-term contracts directly with foundries is becoming increasingly critical to managing supply chain risks.

Key technical terms to understand:

HBM (High-Bandwidth Memory): Stacked DRAM providing high throughput for AI workloads; among the most constrained components

GPU clusters: Networked groups of graphics processing units for parallel AI computation

Inference hardware: Systems optimized for running trained AI models, distinct from training hardware that builds those models

Operational Cost Implications and Their Reflection in Semiconductor Stocks and the Stock Market

Hardware budget increases of 40-80% for AI infrastructure projects have become common. One storage vendor reported approximately 70% average product price increases since early 2026, while input component costs—CPUs, DRAM, Flash—rose 300-900% since mid-2025. These cost escalations affect project ROI calculations and business case development across the broader market.

Power infrastructure upgrades present additional challenges, requiring 18-24 month planning cycles for MW-scale installations. Permitting, construction, and grid interconnection delays compound hardware procurement timelines, creating multi-year project dependencies that traditional IT planning rarely anticipated.

The cost of delays extends beyond hardware: when procurement leads slip, ROI assumptions shift, projects underperform due to lagged deployment, and amortization costs increase. Technology investments that made sense at original cost projections may become questionable at elevated hardware prices.

Technology Architecture Decisions in the Context of AI Infrastructure and Market Volatility

Cloud versus on-premise trade-offs shift significantly under hardware scarcity. Cloud models may provide resilience when on-premise hardware is constrained, but cloud providers themselves face supply constraints—Alibaba’s GPU service prices rose 25-34% due to AI demand and hardware costs. The big four hyperscalers (AWS, Azure, Google Cloud, Meta) are forecast to increase AI infrastructure spend approximately 36% year-over-year to $527 billion in 2026, consuming substantial available capacity.

Hybrid deployment strategies help manage supply chain risk by distributing workloads across environments. Critical latency-sensitive inference operations may run on-premise while training workloads execute in cloud or co-location facilities where hardware capacity is less constrained.

Vendor-agnostic software architecture reduces dependency on specific accelerators. Building abstraction layers that support multiple GPU and AI accelerator vendors improves flexibility when particular hardware becomes unavailable. This approach increases complexity but provides essential risk management benefits.

Key points from this section: Procurement timelines have extended 6-12x, costs have increased 40-80%, and architecture decisions must now factor supply chain resilience alongside traditional performance and cost considerations. These challenges require systematic risk management frameworks.

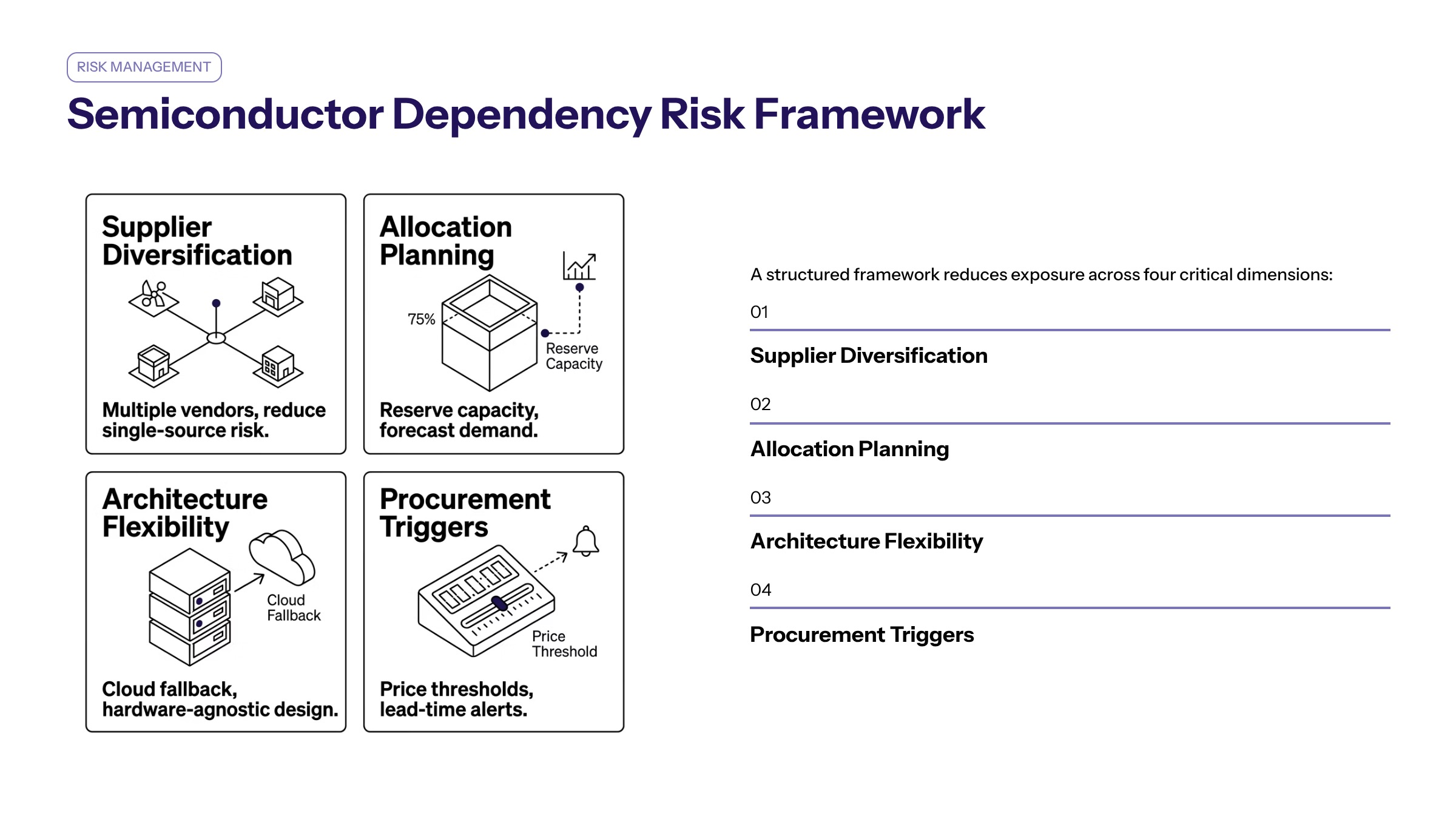

Risk Management Strategies for Semiconductor Dependencies in AI Hardware Demand and Business Risk Mitigation

Building on the operational challenges outlined above, enterprises need structured approaches to semiconductor risk management. Severe supply constraints in the semiconductor industry have transitioned risks from cyclical temporary shortages to permanent structural reliance on a few key suppliers. Systematic frameworks help organizations respond proactively rather than reactively to market volatility.

Supply Chain Diversification Framework to Mitigate Semiconductor Volatility Business Risk

Implement diversification strategies when lead times exceed historical norms or when single suppliers account for more than 40% of critical component spend. The following steps provide a structured implementation approach:

Audit current semiconductor dependencies across your hardware portfolio—identify every server, accelerator, and storage system, mapping critical components that are both essential to operations and supply-constrained (HBM, CoWoS packaging, advanced node GPUs)

Identify alternative suppliers and compatible hardware specifications for each critical component category, including regional foundries and OSATs (Outsourced Semiconductor Assembly and Test)

Establish preferred vendor relationships with 2-3 suppliers per component category, negotiating long-term allocation agreements or pricing floor/ceiling contracts

Create procurement triggers based on lead time and pricing thresholds—define internal benchmarks at which action is required (e.g., when lead times exceed N weeks or price increases surpass X%, open alternative bids or adjust architecture)

Geopolitical tensions and a concentration of advanced chip manufacturing create a fragile supply chain for semiconductor production. Maintaining relationships with geographically diverse suppliers provides resilience against regional disruptions. The CHIPS Act, passed in 2022, authorized approximately $52.7 billion for semiconductor research and manufacturing, along with $39 billion in subsidies for domestic chip manufacturing, aiming to enhance U.S. leadership in technology and innovation—potentially expanding domestic supply options over time.

Technology Architecture Resilience and Business Risk Reduction

Criterion | Cloud-First Model | Hybrid Deployment Model |

|---|---|---|

Hardware procurement risk | Lower (provider absorbs) | Moderate (shared responsibility) |

Cost predictability | Variable (provider pricing) | Mixed (capex + opex blend) |

Performance control | Limited | High for on-premise workloads |

Vendor lock-in risk | Higher | Moderate with abstraction layers |

Supply shortage resilience | Depends on provider capacity | Distributed across environments |

Criterion | Hardware-Specific Architecture | Vendor-Agnostic Architecture |

--------------------------- | --------------------------------- | -------------------------------- |

Implementation complexity | Lower | Higher |

Procurement flexibility | Limited | High |

Performance optimization | Maximized for specific hardware | Some overhead from abstraction |

Risk exposure | Concentrated | Distributed |

Long-term adaptability | Requires migration for changes | Accommodates supplier shifts |

Enterprises should choose based on risk tolerance and operational requirements. Organizations with high availability requirements and limited procurement flexibility benefit from hybrid models. Those with strong vendor relationships and stable supply may optimize with hardware-specific architectures while maintaining migration capabilities. |

Following the passage of the CHIPS Act, companies like Micron announced plans to invest heavily in semiconductor manufacturing, with Micron committing to a $40 billion investment by the end of 2030, indicating a strong response to the incentives provided by the Act. Over time, these investments may expand supply options, though near-term constraints will persist.

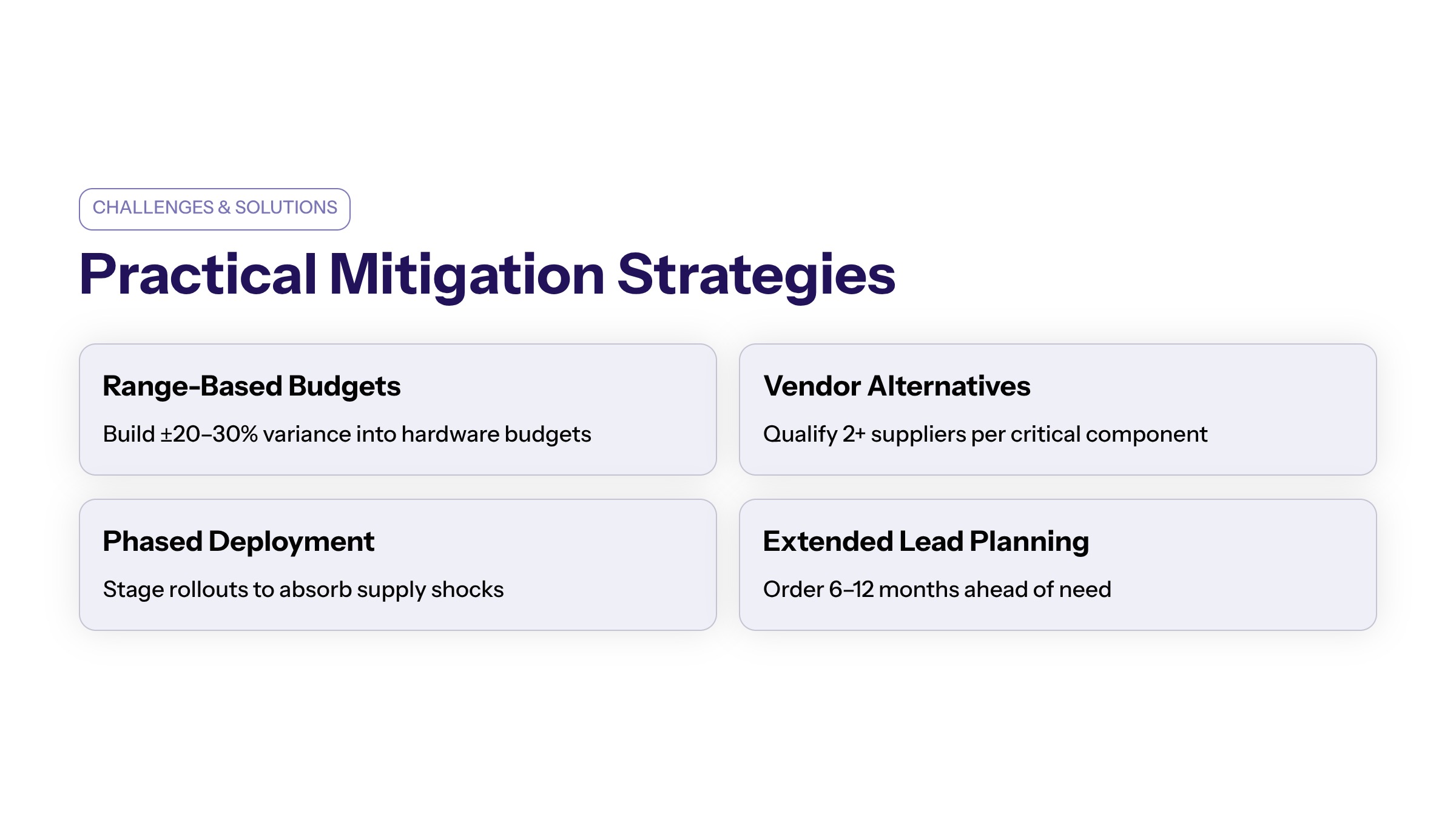

Common Challenges and Solutions for Managing Semiconductor Volatility and AI Hardware Demand Business Risk

Technology teams implementing these strategies encounter recurring obstacles. The following solutions address the most frequent challenges reported by enterprise technology leaders managing semiconductor dependencies.

Budget Approval for Volatile Hardware Costs and Market Volatility Impact

Traditional budgeting based on historical procurement cycles underestimates costs by 40-80% for AI infrastructure under current market conditions.

Solution: Implement range-based budgeting with 20-30% contingency allocations and quarterly cost reviews. Include inflationary indexing or escalation clauses in supplier contracts. Tie project approval milestones to hardware procurement lock-in—commit when vendor quotes are secured rather than when budget is initially allocated.

Vendor Lock-in During Supply Shortages and Stock Market Concentration Risks

Market analysts have noted that the reliance on AI-related stocks has created a crowded trade, which can amplify volatility; if the AI theme falters, many investors may face significant losses due to their concentrated positions. Similar dynamics affect enterprise hardware procurement—concentration on single vendors creates operational risk.

Solution: Negotiate allocation agreements with exit clauses and maintain relationships with 2-3 primary suppliers per component category. Ensure support for multi-vendor compatibility in hardware specifications. Consider maintaining strategic inventory for critical components where cost and obsolescence risk justify the investment.

Project Timeline Management with Extended Lead Times and Business Impact

Lead times exceeding 50 weeks for cutting-edge components require fundamentally different project planning approaches.

Solution: Adopt phased deployment approaches and parallel hardware procurement for critical path projects. Order critical components early while postponing non-essential elements. Place overlapping orders with different vendors or for different configurations to hedge against allocation failures. Schedule procurement milestones well ahead of deployment deadlines with built-in slack time.

The implementation of the CHIPS Act has been shown to significantly reduce downside risk in the stock prices of semiconductor firms that are directly exposed to its benefits, compared to those that are not—suggesting that policy developments can affect long-term supply stability. The CHIPS Act may increase market risk while also having the potential to boost market returns, as it encourages significant investments in semiconductor manufacturing and research.

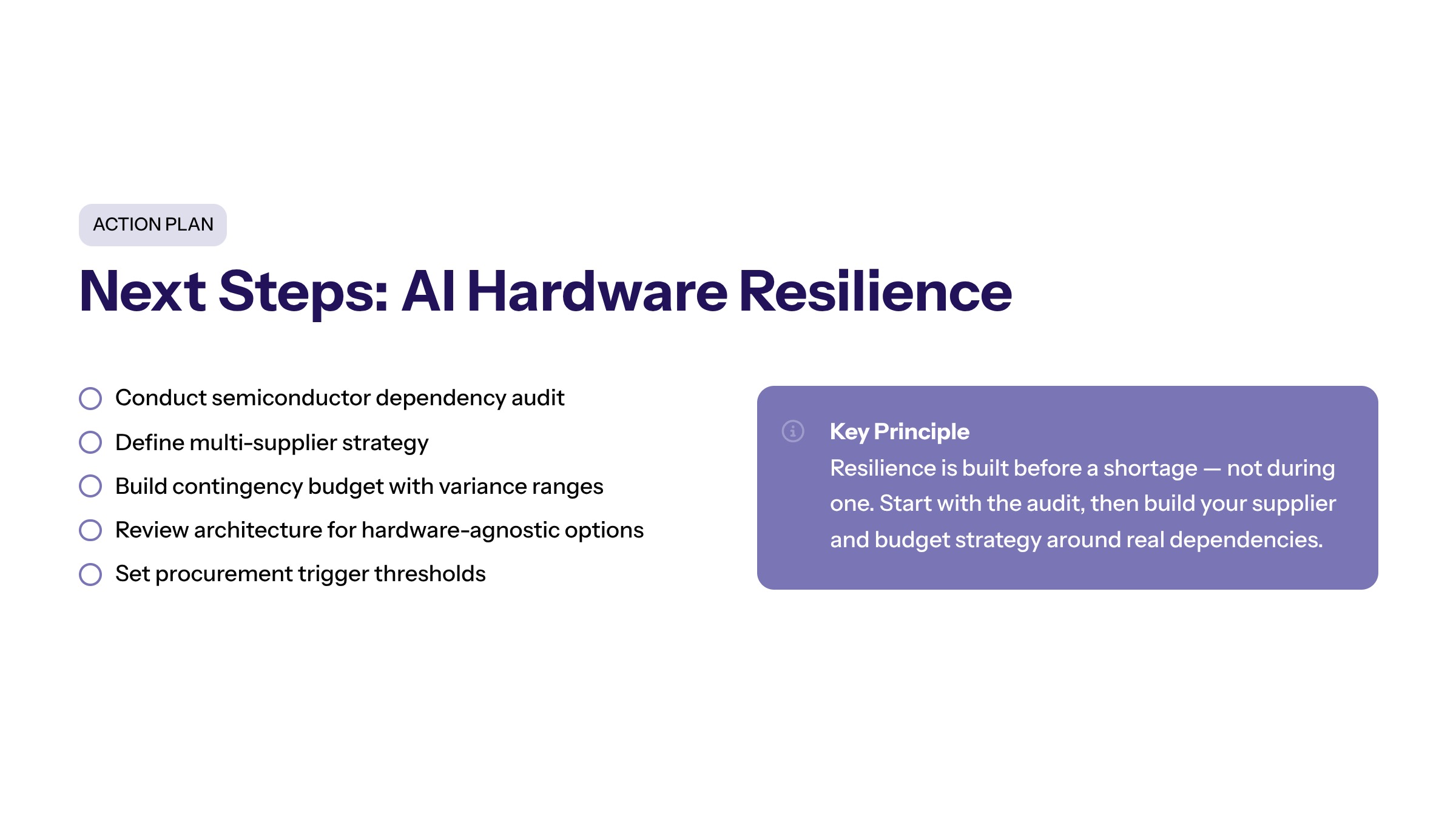

Conclusion and Next Steps

Semiconductor volatility requires proactive risk management and flexible technology architecture. The structural tightness in AI hardware supply is expected to persist through 2026 into 2027, especially for HBM, CoWoS packaging, and advanced logic nodes. Organizations that move early—conducting audits, securing supplier commitments, and investing in software flexibility—will avoid the worst cost escalations and delays.

Conduct a comprehensive dependency audit identifying all semiconductor-constrained components in your hardware portfolio

Establish or strengthen relationships with 2-3 suppliers per critical component category

Implement range-based budgeting with 20-30% contingency for hardware-intensive projects

Evaluate current architecture for vendor lock-in risk and implement abstraction layers where feasible

Develop procurement triggers and escalation procedures for lead time and pricing thresholds

Related topics worth exploring: Cloud migration strategies that balance cost optimization with supply chain resilience, vendor management frameworks for strategic technology partnerships, and technology portfolio optimization approaches that reduce overall hardware intensity while maintaining AI capabilities.

The CHIPS Act has led to a notable increase in stock buyback announcements among semiconductor firms, which could distort financial markets if not managed properly, as companies are prohibited from using CHIPS Act grants for dividends or stock buybacks. Monitoring policy developments and their effects on supply expansion will remain important for long-term planning.

Organizations that treat semiconductor volatility as a strategic concern—not merely a procurement inconvenience—will maintain competitive advantage as AI infrastructure becomes increasingly central to business operations.