US NVIDIA H200 AI Chip Sales: Market Performance and Industry Impact Analysis

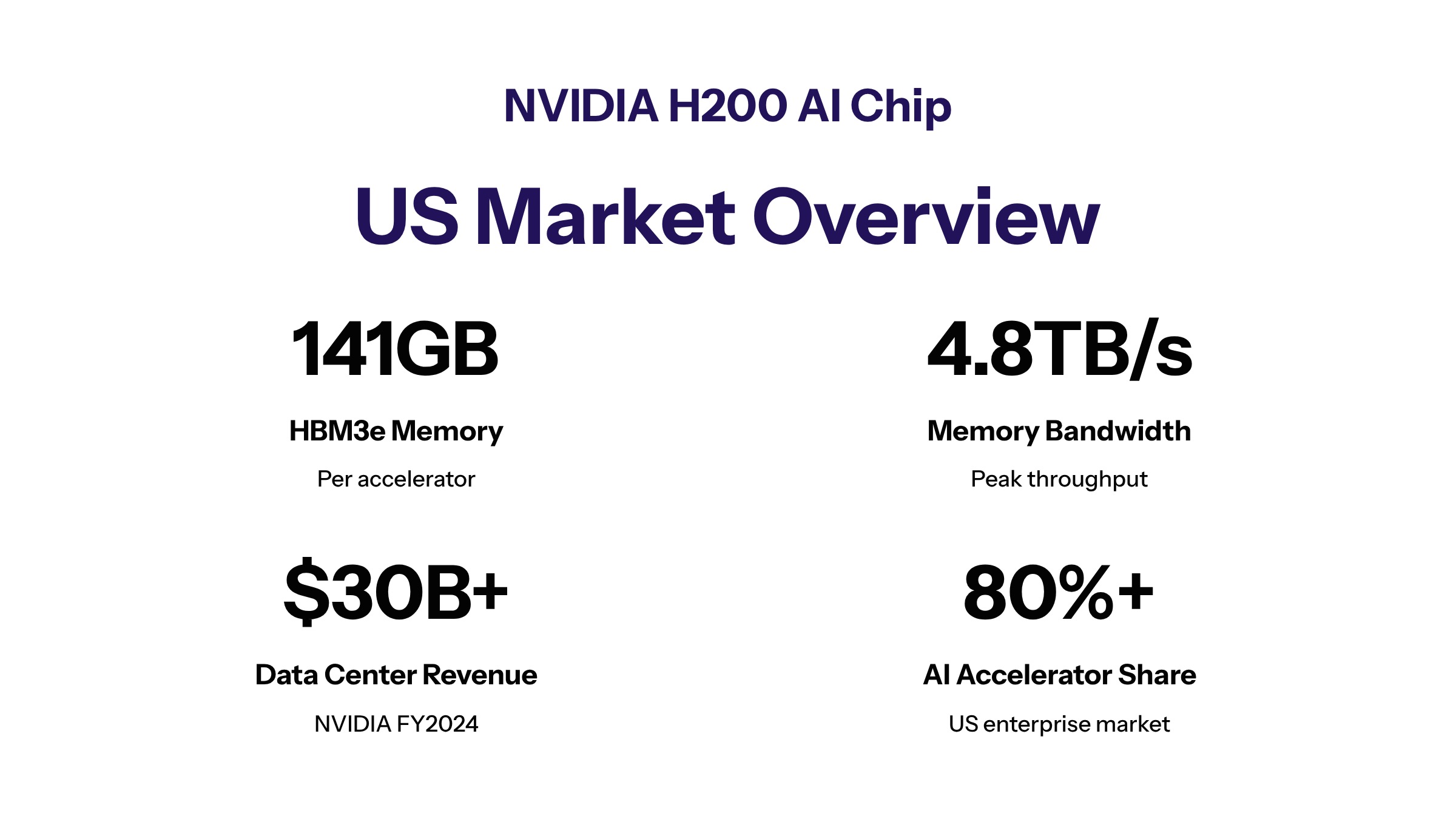

NVIDIA H200 chip sales in the US market represent a cornerstone of the company’s data center dominance, with approximately 1.8 million H200-equivalent compute units deployed in US and non-China markets as of early 2026. The Hopper-generation accelerator has driven substantial revenue growth, contributing to NVIDIA’s record $193.737 billion Data Center segment revenue for fiscal 2026—a 68% year-over-year increase that underscores the chip’s commercial significance.

This analysis covers verified sales data, market penetration metrics, customer adoption patterns, and competitive positioning for the H200 chip specifically within the US market. The scope extends to pricing dynamics, supply chain realities, and regulatory factors but excludes detailed technical benchmarking or comprehensive global market analysis. Enterprise decision-makers evaluating AI infrastructure investments, AI developers selecting hardware backends, technology investors tracking NVIDIA’s data center strategy, and industry analysts monitoring AI compute market dynamics will find actionable intelligence throughout.

To directly address the core question: NVIDIA does not publicly disclose US-only H200 revenue or unit sales separately. However, analysis by Epoch AI and CNAS estimates that roughly 2 million Hopper-class chips (H100 + H200 combined) have been produced globally, with approximately 85% deployed in US or non-China markets. The Data Center segment—where H200 revenue is embedded—generated $62.314 billion in Q4 FY2026 alone.

Key insights readers will gain:

Current H200 sales volume estimates and revenue contribution patterns in the US market

Customer segment breakdown showing which buyers drive domestic H200 demand

Competitive positioning against AMD, Intel, and NVIDIA’s own Blackwell-class successors

Supply chain and policy factors creating procurement challenges and market dynamics

Forward-looking trends as the market transitions toward next-generation architectures

Understanding NVIDIA H200 AI Chip Technology

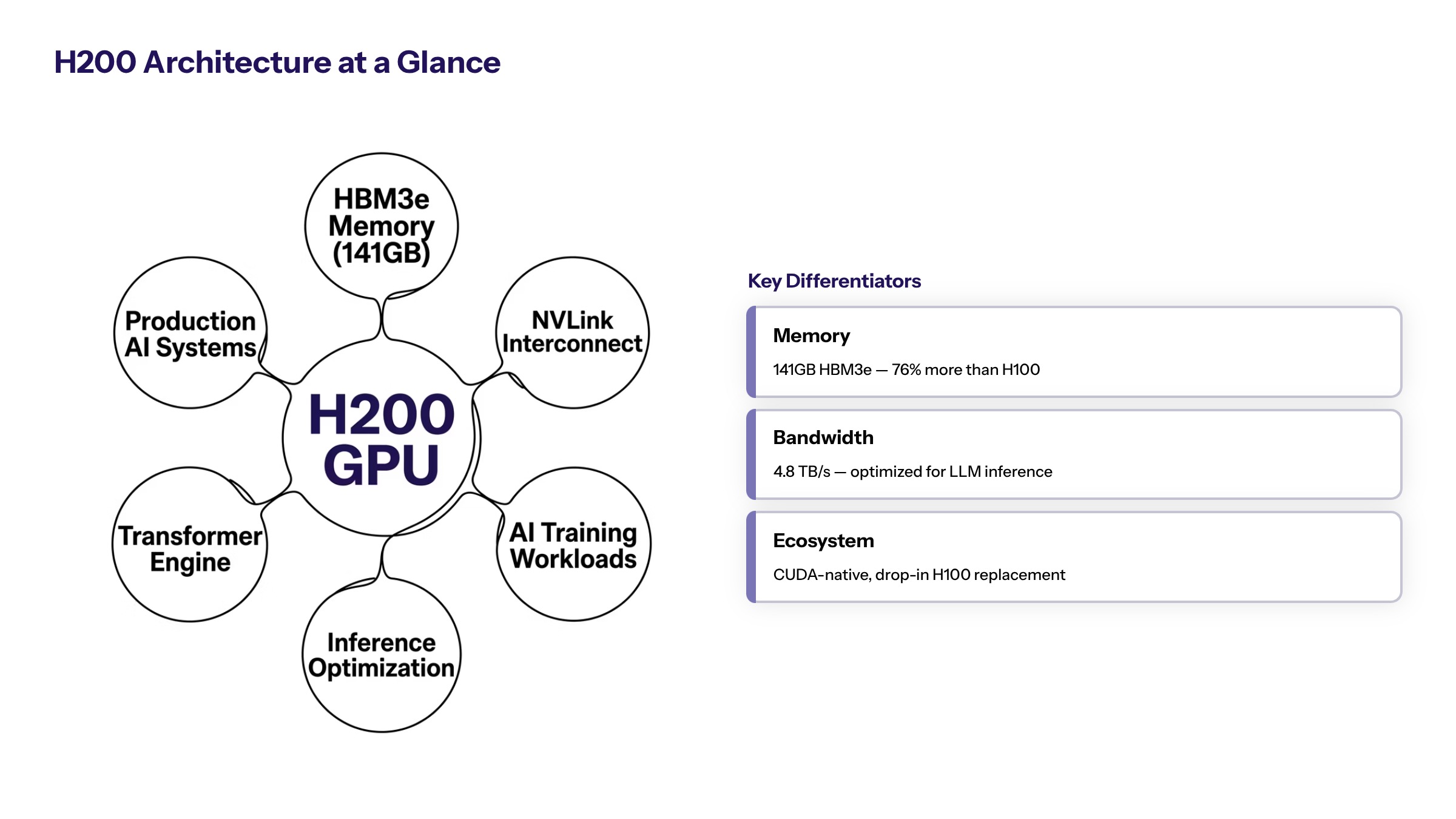

The H200 is NVIDIA’s high-performance Hopper-generation GPU accelerator, featuring approximately 141GB of HBM3e memory and engineered for demanding AI training and inference workloads. This chip represents the performance ceiling for pre-Blackwell architecture, delivering roughly six times the capability of the export-restricted H20 variant while maintaining compatibility with established NVIDIA software ecosystems.

For enterprise AI workloads and data center operations, the H200 matters because it addresses the computational intensity of large foundation models, mixed-precision training, and high-throughput inference serving. Organizations running production AI systems—rather than experimental deployments—require the memory bandwidth and compute density that H200 provides.

H200 Architecture and Performance

The H200 builds on the Hopper architecture with significant memory improvements over its H100 predecessor. The 141GB HBM3e configuration delivers substantially higher memory bandwidth, enabling faster data movement for memory-bound AI workloads. This architectural advantage translates directly to reduced training times for large language models and improved inference latency for production deployments.

These performance characteristics drive enterprise demand because organizations can process larger batch sizes, train bigger models, and serve more concurrent inference requests per chip. The connection between technical specifications and purchasing decisions becomes clear when enterprises calculate total cost of ownership: fewer H200 chips may accomplish what requires more units of competing or previous-generation hardware.

Target Applications and Use Cases

Primary enterprise applications driving H200 adoption include large-scale model training for hyperscalers and cloud providers, inference serving for AI-powered products, and specialized on-premises deployments for data-sensitive industries. A notable example illustrates this shift: a US manufacturer installed on-site H200 GPU clusters for production-floor AI applications including quality control and supply planning, demonstrating the transition from cloud-dependent pilots to dedicated local infrastructure.

The relationship between chip capabilities and customer purchasing decisions reflects workload requirements. Organizations with latency-sensitive applications, data sovereignty concerns, or regulatory compliance obligations increasingly view H200 procurement as infrastructure investment rather than experimental spending. This procurement mindset bridges technical features to market demand patterns, setting the stage for examining actual sales performance.

US Market Sales Performance Analysis

Building on the technical foundation, sales data reveals how H200 capabilities translate into commercial results across the US market.

Q4 2025 and Q1 2026 Sales Figures

NVIDIA’s Data Center revenue reached $62.314 billion in Q4 FY2026, comprising compute hardware and networking products. While the company does not break out H200-specific revenue, analysts estimate that Hopper-class chips contributed significantly to this figure during their peak sales period. The overall Data Center segment grew approximately 68% year-over-year for fiscal 2026, reflecting sustained enterprise demand for AI accelerators.

Blackwell architecture revenue grew sequentially by approximately 17% in recent quarters, indicating that buyers are proceeding with newer chip purchases as availability improves. This transition suggests H200 shipments peaked in 2024 and early 2025, with estimates indicating roughly 85% of Hopper shipments during this period were H200 units rather than H100 variants.

Customer Segments and Adoption Rates

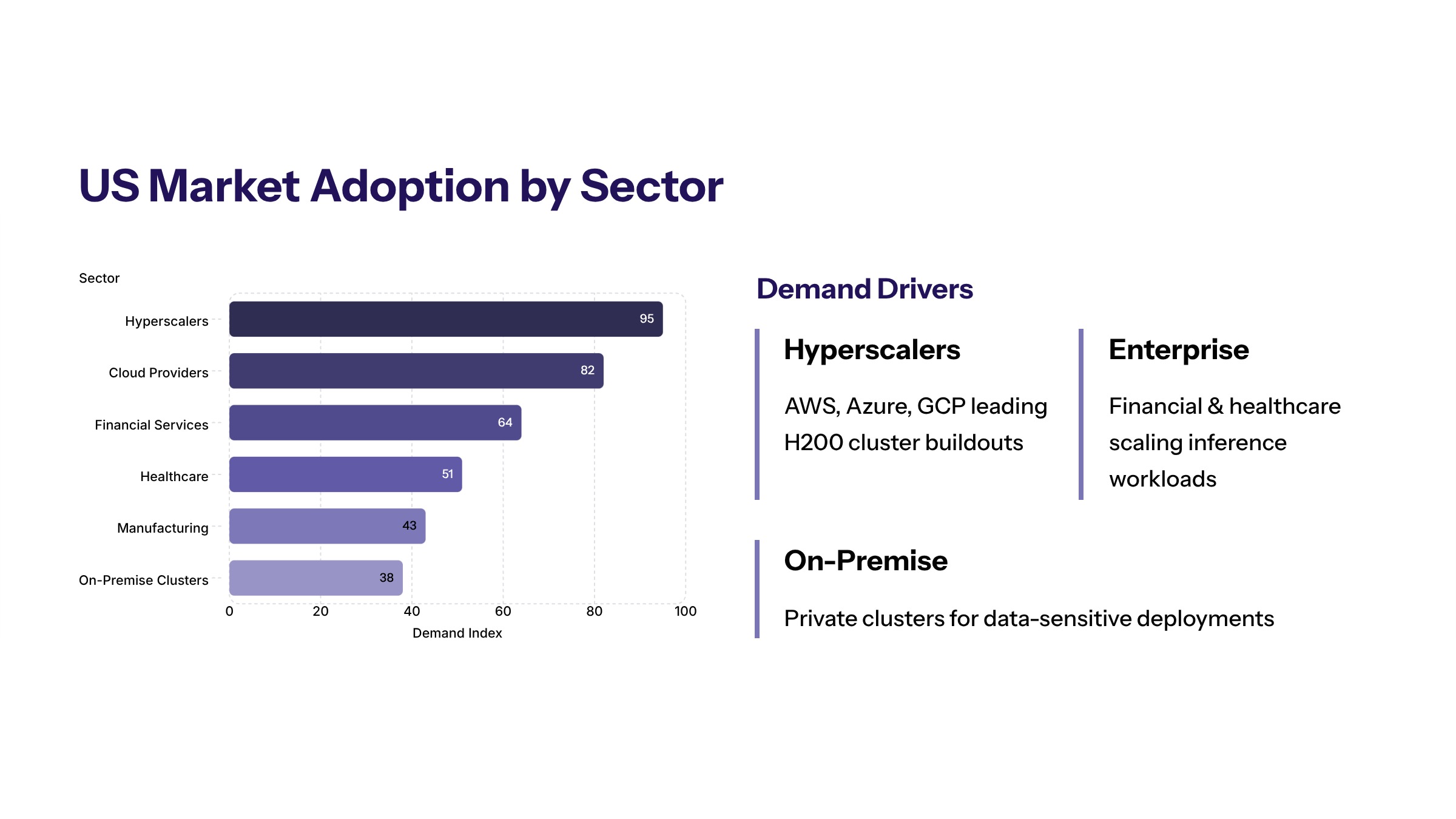

Major US hyperscalers and cloud providers remain the primary H200 buyers, accounting for the majority of domestic chip sales. According to Epoch AI’s analysis, hyperscalers own most leading AI chips globally, with Chinese customers representing only approximately 5% of global compute—implying that most H200 units are installed in US cloud and data center settings.

Enterprise adoption beyond hyperscalers continues expanding, particularly among organizations with specialized requirements. Manufacturing, financial services, and healthcare enterprises increasingly deploy H200 clusters on-premises for workloads where latency, data privacy, or compliance requirements justify the capital investment over cloud alternatives.

Pricing Trends and Market Dynamics

Average selling price per H200 chip remains undisclosed, though Hopper-class accelerators command premium pricing among AI accelerators. Epoch AI models allocate revenue across hardware variants to estimate pricing, but specific figures are proprietary. The high per-unit cost creates procurement barriers that only well-capitalized enterprises can clear.

Market dynamics shifted as Blackwell-class chips entered production. H200’s relative value proposition changes when newer architecture offers superior performance per watt and potentially better cost efficiency for equivalent workloads. Supply constraints in HBM3e memory and TSMC CoWoS packaging capacity continue influencing production ramp rates, creating availability challenges that matter for enterprise procurement planning.

Sales Data and Competitive Market Impact

This section builds on sales performance data to examine competitive positioning and market share implications for enterprise investment and procurement decisions.

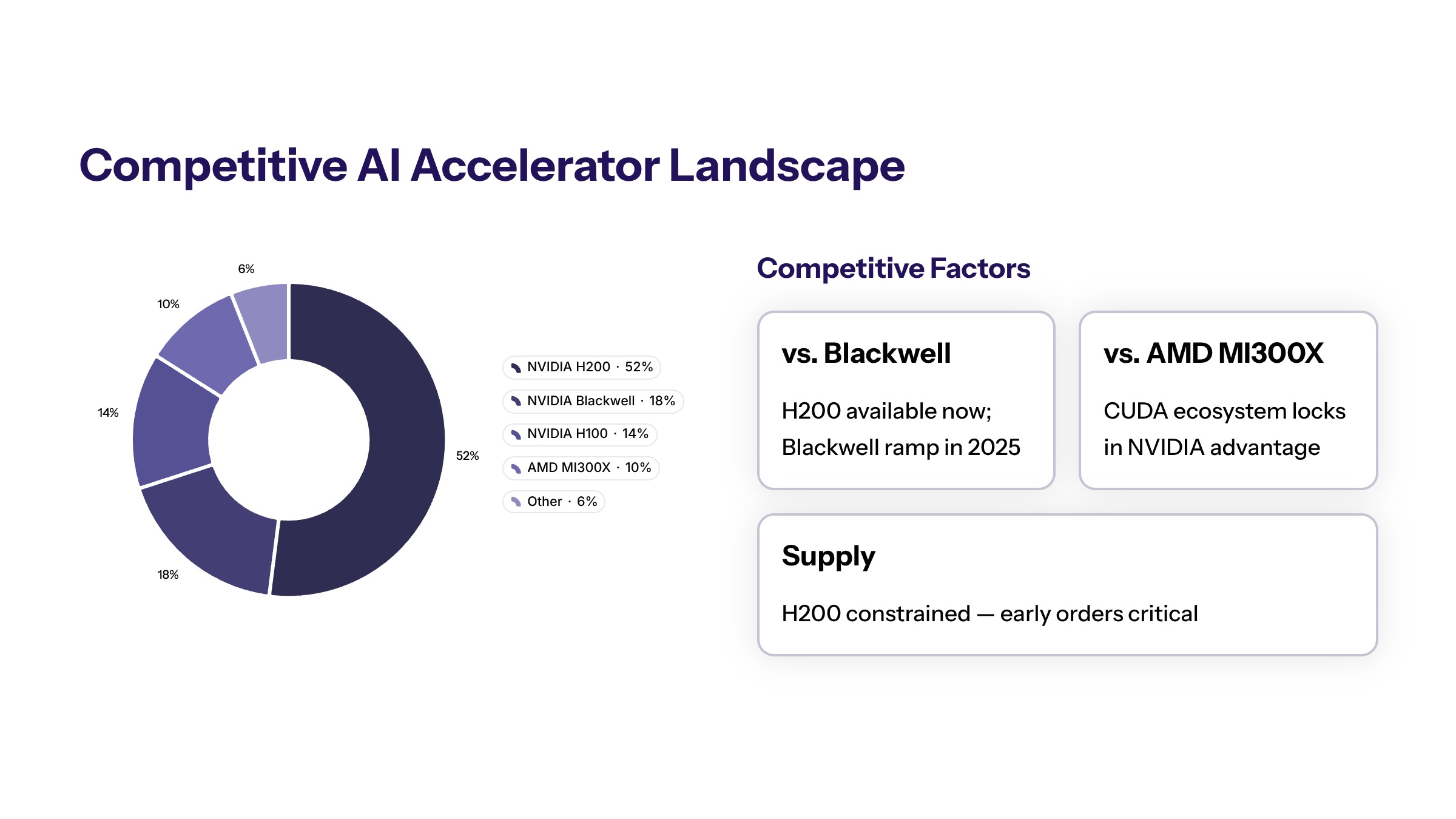

Market Share Analysis

NVIDIA maintains dominant market share in AI accelerators, with H200 competing primarily against AMD’s MI325X and Intel AI chip alternatives. In export policy discussions, US regulators consider AMD’s MI325X alongside H200 when establishing licensing requirements—indicating comparable market positioning from a capability standpoint.

Customer preference factors driving H200 selection include software ecosystem maturity (CUDA dominance), enterprise support infrastructure, and established deployment patterns. Organizations already invested in NVIDIA tooling face switching costs that reinforce vendor loyalty, even when competitors offer compelling price-performance alternatives.

Supply chain and availability dynamics significantly impact sales performance. When export restrictions to China disrupted production planning, H200 manufacturing capacity was reallocated or paused for extended periods. Production restarts following policy clarification in late 2025 and early 2026 are still catching up to full-scale manufacturing targets.

Revenue contribution to NVIDIA’s overall data center business remains substantial, though the exact H200 proportion is undisclosed. Analysts estimate tens of billions in annual H200 revenue during peak periods, embedded within the broader Data Center segment figures.

Sales Performance Comparison

Criterion | H200 | H100 | Blackwell (B200) | AMD MI325X |

|---|---|---|---|---|

Estimated Global Shipments | ~2M Hopper units combined | Included in Hopper estimate | Early ramp phase | Not publicly disclosed |

US/Non-China Market Share | ~85% of shipments | Declining as H200 replaced | Growing rapidly | Smaller but expanding |

Memory Configuration | ~141GB HBM3e | 80GB HBM3 | Higher than H200 | Competitive with H200 |

Market Position | Mature, peak sales passed | Legacy | Future growth driver | Challenger positioning |

Supply Status | Stabilizing | Limited new production | Ramping with constraints | Available |

This comparison helps enterprise decision-makers interpret competitive positioning. H200 represents mature technology with established support, while Blackwell offers future-proofing at premium pricing and availability constraints. AMD alternatives solve specific use cases but face ecosystem adoption challenges. The market trends clearly show Blackwell capturing incremental growth while H200 maintains installed base value.

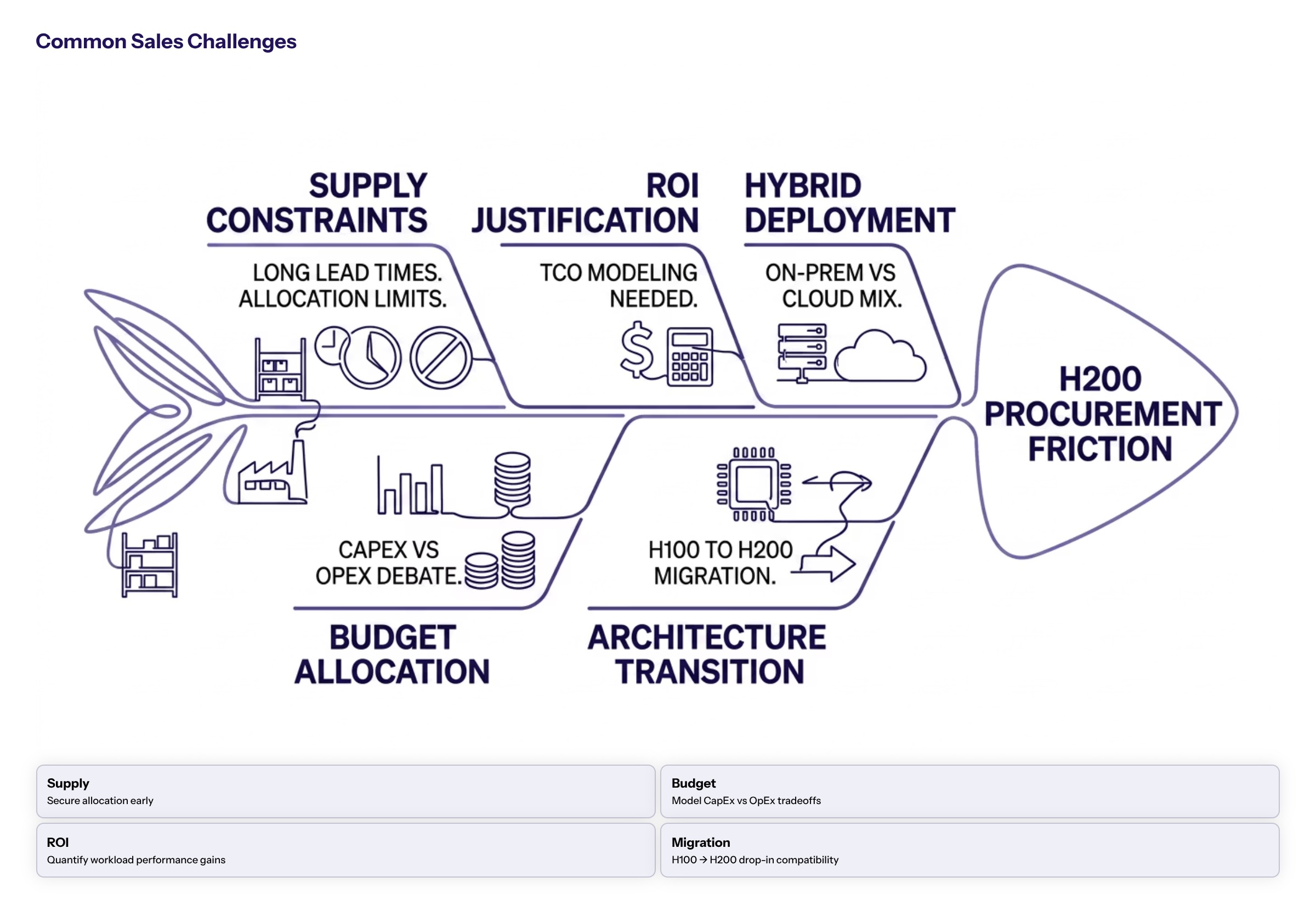

Common Sales Challenges and Market Solutions

Enterprise procurement and market dynamics create distinct challenges that affect H200 availability, affordability, and competitive selection.

Supply Chain Constraints

Current manufacturing capacity limitations continue affecting H200 availability despite production restarts. The primary constraints involve HBM3e memory supply, TSMC CoWoS packaging capacity, and fab production throughput. When export policy changes imposed restrictions, production for H200 was largely paused or rerouted, creating backlogs that persist into 2026.

NVIDIA’s production scaling strategies include diversifying packaging suppliers and working with memory vendors to increase HBM3e output. Timeline expectations suggest supply normalization throughout 2026, though enterprise buyers should account for 3-6 month lead times for large orders.

Enterprise Budget Allocation

High per-unit cost challenges require enterprise ROI justification that goes beyond chip pricing. Total cost of ownership calculations must include power consumption (significant for H200), cooling infrastructure, networking requirements, and software stack licensing. Organizations increasingly create business cases that quantify model performance improvements, inference cost reductions, and competitive advantages from AI capabilities.

Financing and procurement strategies organizations use for H200 purchases include cloud credits for burst capacity, reserved instance commitments, and hybrid deployment models that balance capital expenditure with operational flexibility. Some enterprises mitigate cost risk by deploying H200 for specific workload islands rather than full-fleet standardization.

Competitive Pressure from AMD and Intel

Market competition from AMD and Intel influences H200 sales strategy and pricing adjustments, particularly for cost-sensitive buyers. AMD’s MI325X offers competitive performance in specific workloads, creating legitimate alternatives that procurement teams must evaluate. Intel continues developing AI accelerators, though market penetration remains limited.

However, the more significant competitive pressure comes from NVIDIA’s own Blackwell architecture. As B200 and GB200 chips ramp production, many new orders bypass H200 entirely, reducing long-term growth potential for the older architecture. Enterprises waiting for Blackwell availability may delay H200 purchases, creating a transitional market dynamic.

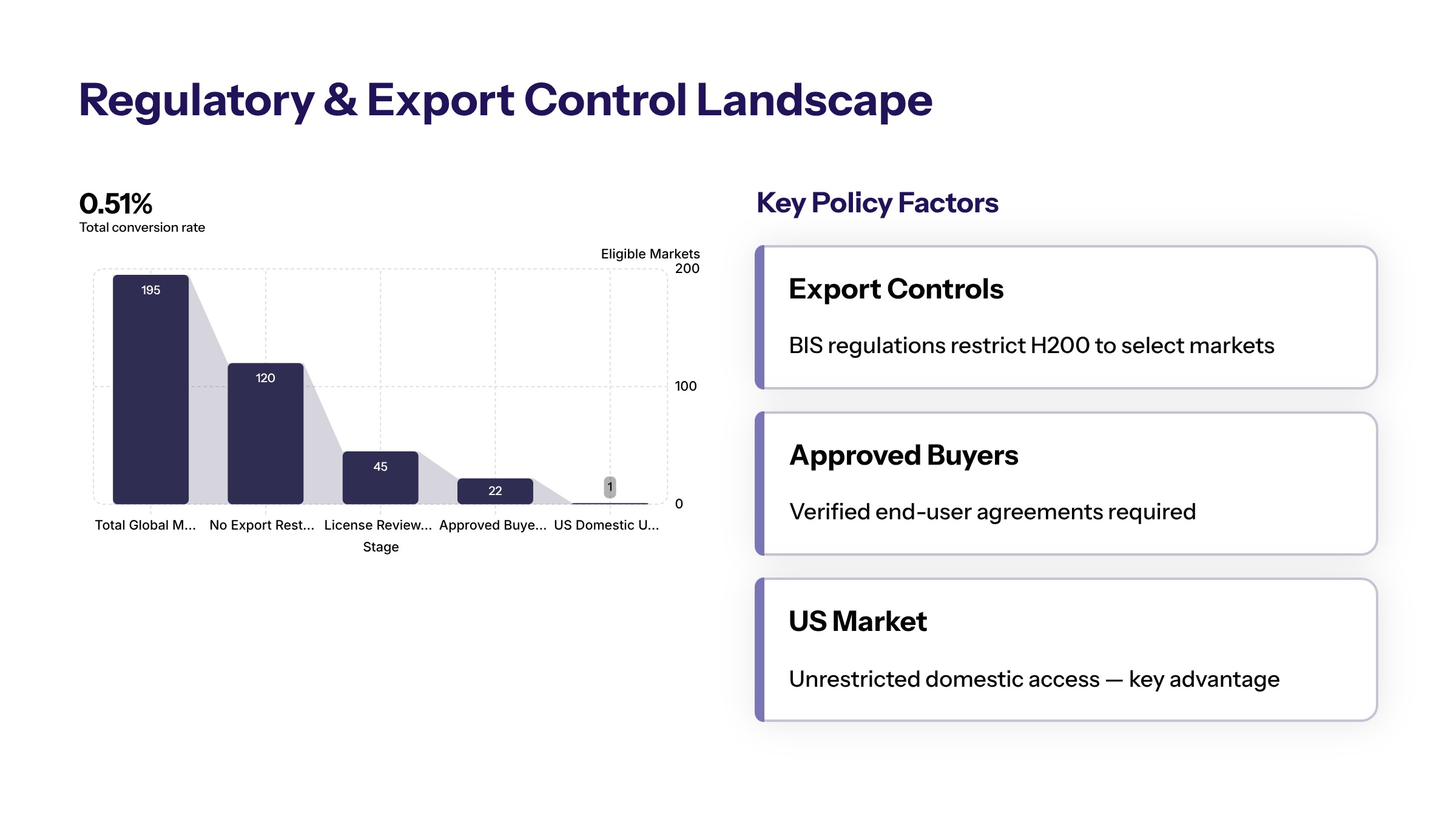

H200 Chip Sales and Regulatory Approvals

This section examines the recent developments in H200 chip sales, focusing on regulatory clearances and the impact on international market access, particularly concerning Chinese firms.

Chip Sales to 10 Approved Chinese Firms

In a significant policy breakthrough, the US clears sales of NVIDIA's H200 AI chips to 10 Chinese firms, marking a notable shift in export controls. This approval allows major Chinese technology companies, including Alibaba, to buy and integrate H200 chips into their AI infrastructure. The decision reflects careful balancing of national security concerns with commercial interests, enabling these firms to access cutting-edge AI hardware while maintaining regulatory oversight.

Impact on 10 Chinese Firms and Market Dynamics

The authorization for chip sales to 10 Chinese firms is expected to accelerate AI development and deployment within China, enhancing competitive positioning in the global AI race. Firms like Alibaba will leverage the H200’s advanced capabilities for large-scale model training and inference applications. This move also signals potential easing of restrictions, fostering broader collaboration opportunities. Industry news highlights this as a breakthrough moment, influencing procurement strategies and prompting other Chinese enterprises to consider acquiring NVIDIA’s AI chips under the new regulatory framework.

Conclusion and Next Steps

The H200 represents NVIDIA’s high-water mark for pre-Blackwell AI acceleration, with approximately 1.8 million compute-equivalent units deployed in US and non-China markets contributing substantially to the company’s record data center revenue. While NVIDIA does not disclose US-specific H200 sales figures, the chip’s role in driving 68% year-over-year Data Center growth demonstrates its commercial significance. Market dynamics now favor Blackwell adoption for new deployments, though H200 maintains value for enterprises with immediate requirements or established Hopper investments.

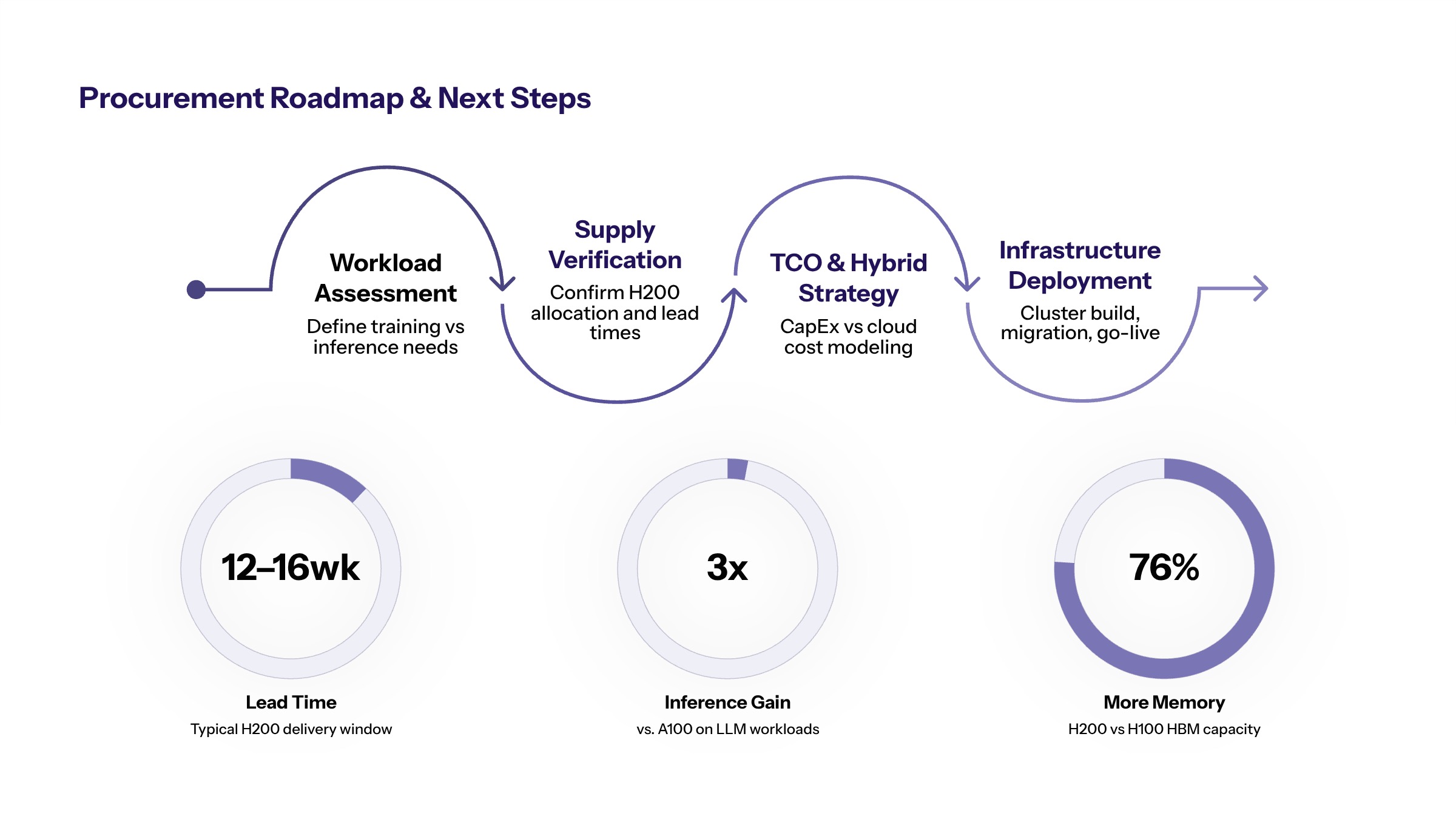

Immediate actionable next steps for enterprise decision-makers considering H200 procurement:

Evaluate workload timelines—projects completing within 12-18 months may justify H200, while longer horizons favor waiting for Blackwell availability

Assess total cost of ownership including infrastructure requirements, not just chip pricing

Verify supply availability and lead times with NVIDIA or authorized partners before finalizing procurement plans

Consider hybrid strategies combining cloud bursts with strategic on-premises deployments

Related topics worth exploring include NVIDIA’s Blackwell and Rubin architecture roadmaps, AI infrastructure planning frameworks that align hardware investments with business outcomes, and competitive analysis of AMD and Intel alternatives for specific workload profiles.

Additional Resources

NVIDIA Investor Relations quarterly earnings reports containing Data Center segment revenue breakdowns

Epoch AI’s AI Chip Sales documentation and Chip Owners Explorer for shipment estimates and market analysis

CNAS policy analysis on H200 export controls and market distribution patterns

Industry analyst reports from Google and Reuters covering AI chip market trends and competitive dynamics