AI Workflow Automation for Finance: Use Cases, Controls, and Implementation

AI workflow automation for finance uses AI to support finance workflows such as review, routing, reconciliation support, exception handling, document processing, and reporting. For finance teams, the goal is not to remove accountability. The goal is to make work more visible, consistent, auditable, and easier to govern.

Finance leaders, CTOs, compliance stakeholders, operations leaders, and financial-services teams evaluating AI workflow automation for finance need a control-first view. Practical planning should cover use cases, implementation challenges, control requirements, responsible AI framing, AI agents in financial workflows, and a cautious implementation roadmap.

Finance AI workflows require clear data access, system integration, approval thresholds, human review, and audit evidence before production use. AI can help classify documents, summarize records, flag exceptions, prepare review notes, and route tasks, but financial decisions and sensitive actions need accountable human ownership.

Finance workflow automation should be treated as operational support, not as a substitute for financial, tax, legal, or compliance review. Teams should design AI workflows around documented policies, approval thresholds, audit trails, and accountable human review.

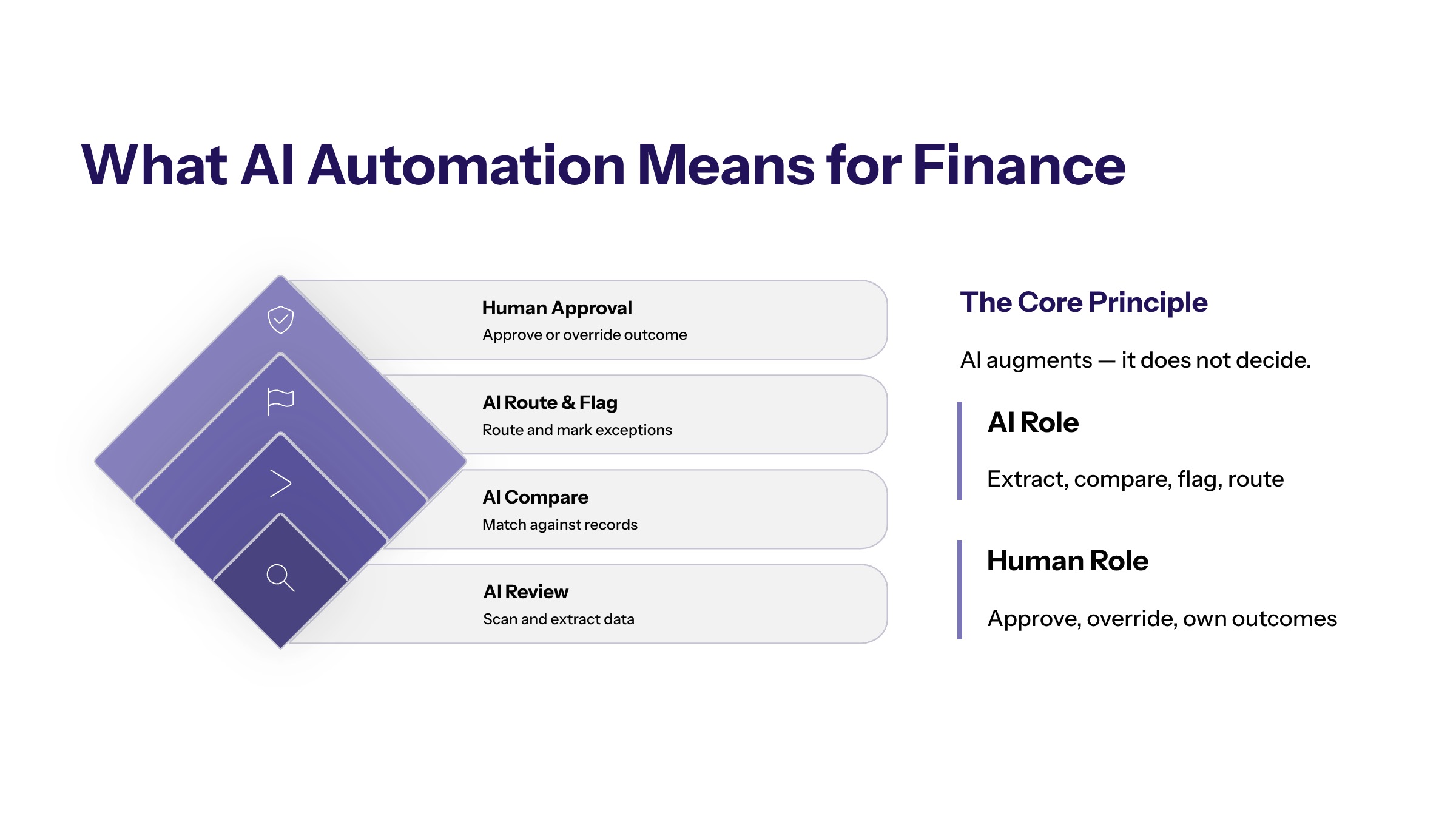

What AI Workflow Automation Means for Finance

Finance workflows often depend on structured records, unstructured documents, approvals, exceptions, and audit evidence. AI workflow automation can help teams interpret documents, compare fields, summarize context, prepare approvals, and route exceptions to the right owner.

The workflow matters more than the model. A finance team may use AI to extract invoice data, but the value comes from what happens next: matching against available records, flagging missing information, routing to an owner, creating an audit trail, and recording the approved outcome.

Finance automation should be designed around control. AI can support the work, but the business must define what the AI can read, what it can recommend, what it can write, and when human approval is required. Without those boundaries, automation can create operational risk.

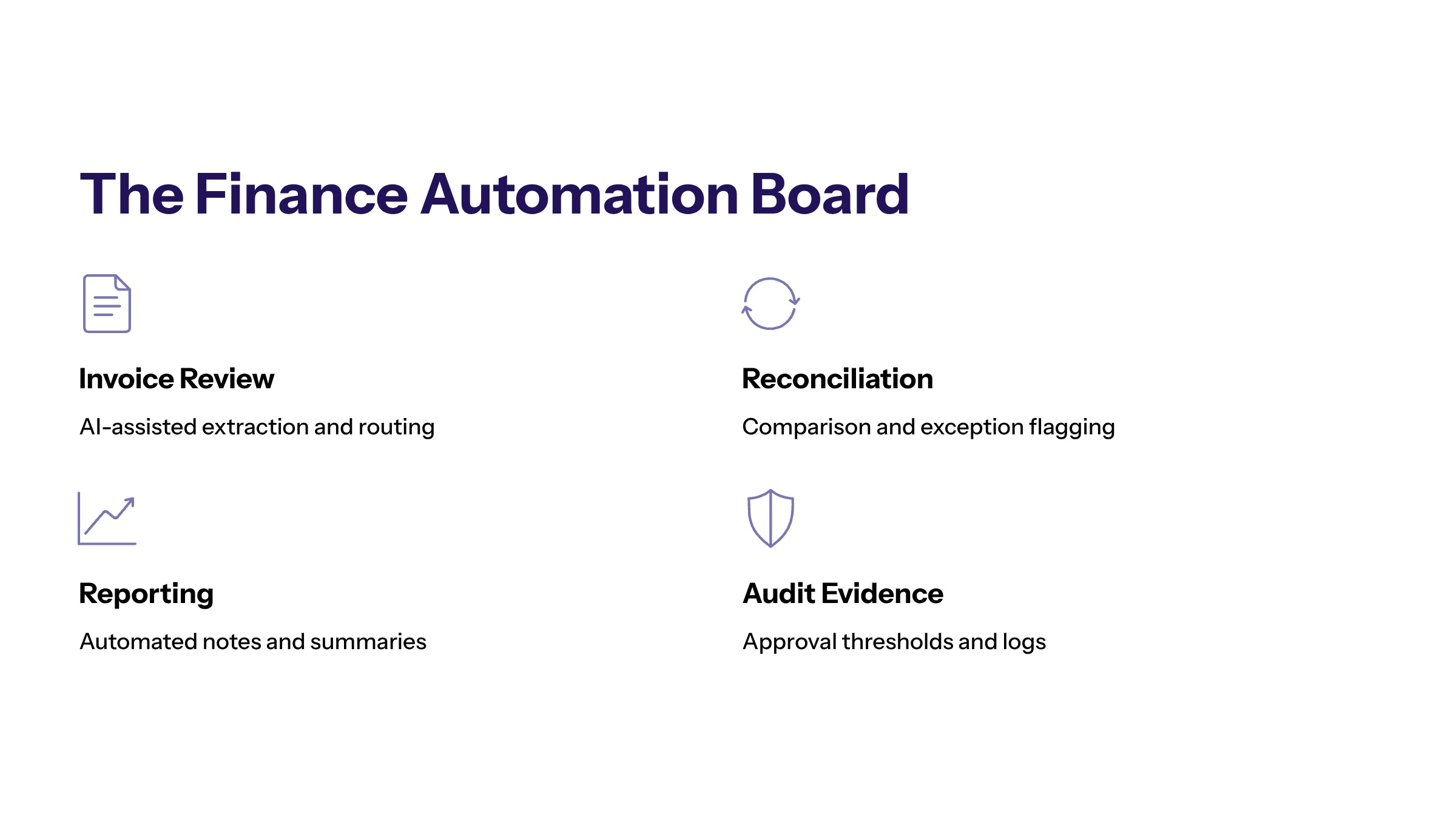

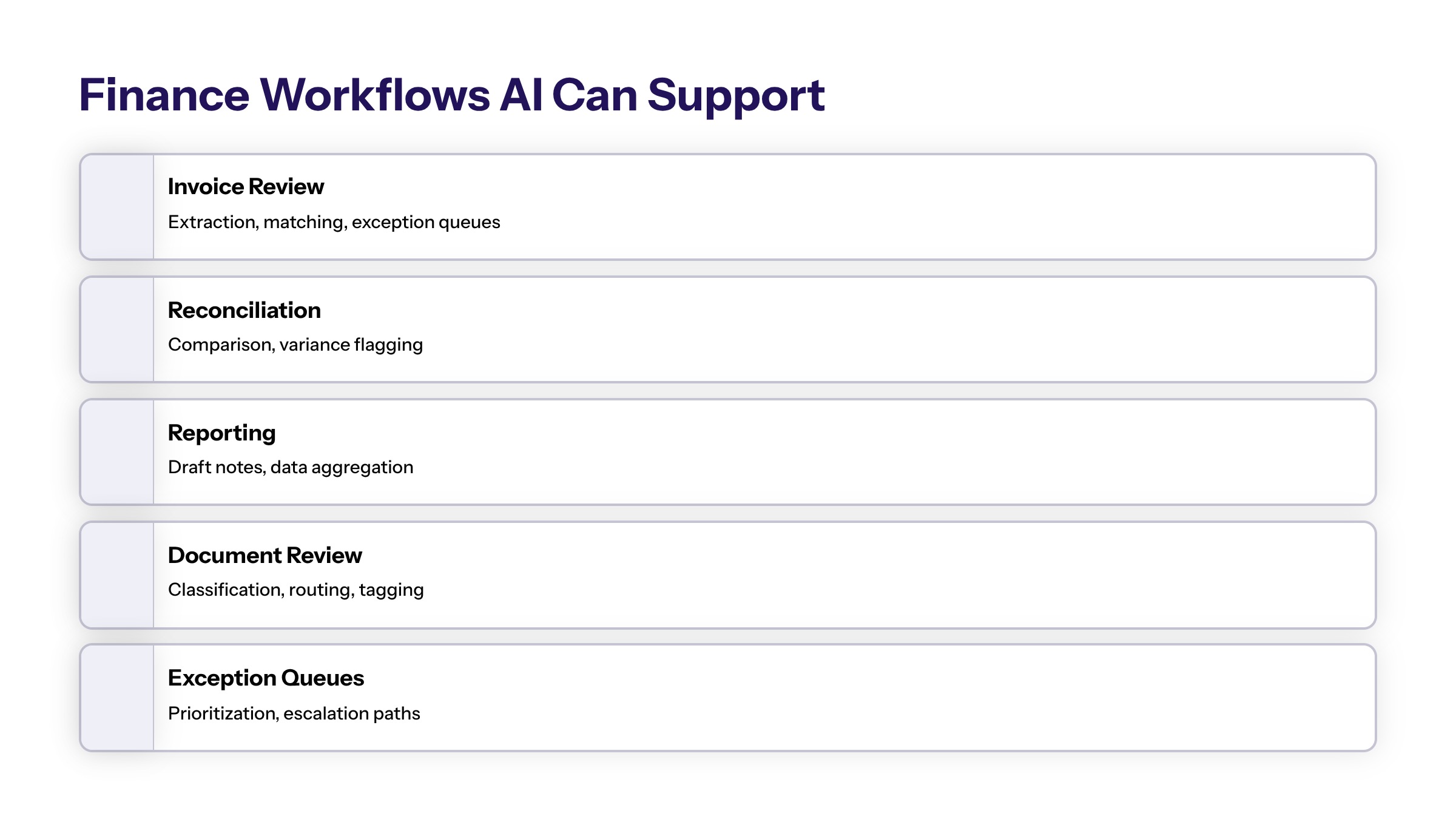

Finance Workflows AI Can Support

AI can support finance workflows where teams repeatedly review information, compare records, prepare notes, or route exceptions. The strongest candidates are bounded workflows with clear owners and measurable process friction.

Finance Workflow | AI Role | Control Requirement | Metric Category |

|---|---|---|---|

Invoice review | Extract fields, compare records, and flag mismatches. | Human approval before payment action. | Approval latency, exception rate, audit evidence. |

Reconciliation support | Identify discrepancies and prepare review notes. | Finance owner validates final resolution. | Manual touches, unresolved exceptions, rework. |

Reporting workflows | Summarize inputs and prepare variance notes. | Reviewer confirms figures and context. | Review cycle time and correction rate. |

Document review | Classify files, extract key fields, and route missing data. | Access controls and audit trails. | Missing-field rate and routing accuracy. |

Exception queues | Prioritize issues and recommend owners. | Escalation path and owner accountability. | Queue age and time to assignment. |

The table keeps the focus on workflow automation, not autonomous finance decisions. Each use case requires a human control point because finance workflows often affect records, approvals, reporting, or sensitive information.

Financial Services AI Implementation Challenges

Financial services AI implementation challenges often begin with data and ownership. Finance workflows may depend on ERP data, accounting records, documents, approvals, customer records, vendor records, reporting tools, and historical notes. If those sources are fragmented, AI output may be incomplete or difficult to trust.

Another challenge is workflow ambiguity. If the current process depends on undocumented judgment or informal escalation, AI automation may expose that weakness. The first step may be workflow mapping and ownership design before any model or tool is selected.

Security and privacy also matter. Finance workflows can involve sensitive business data, personal data, contractual terms, financial records, or customer-impacting information. Access should be limited to what the workflow requires, and actions should be logged.

Finally, AI implementation support services for finance should include ongoing monitoring. Finance workflows change as business rules, systems, policies, and teams change. The operating model must include review, change control, and support after launch.

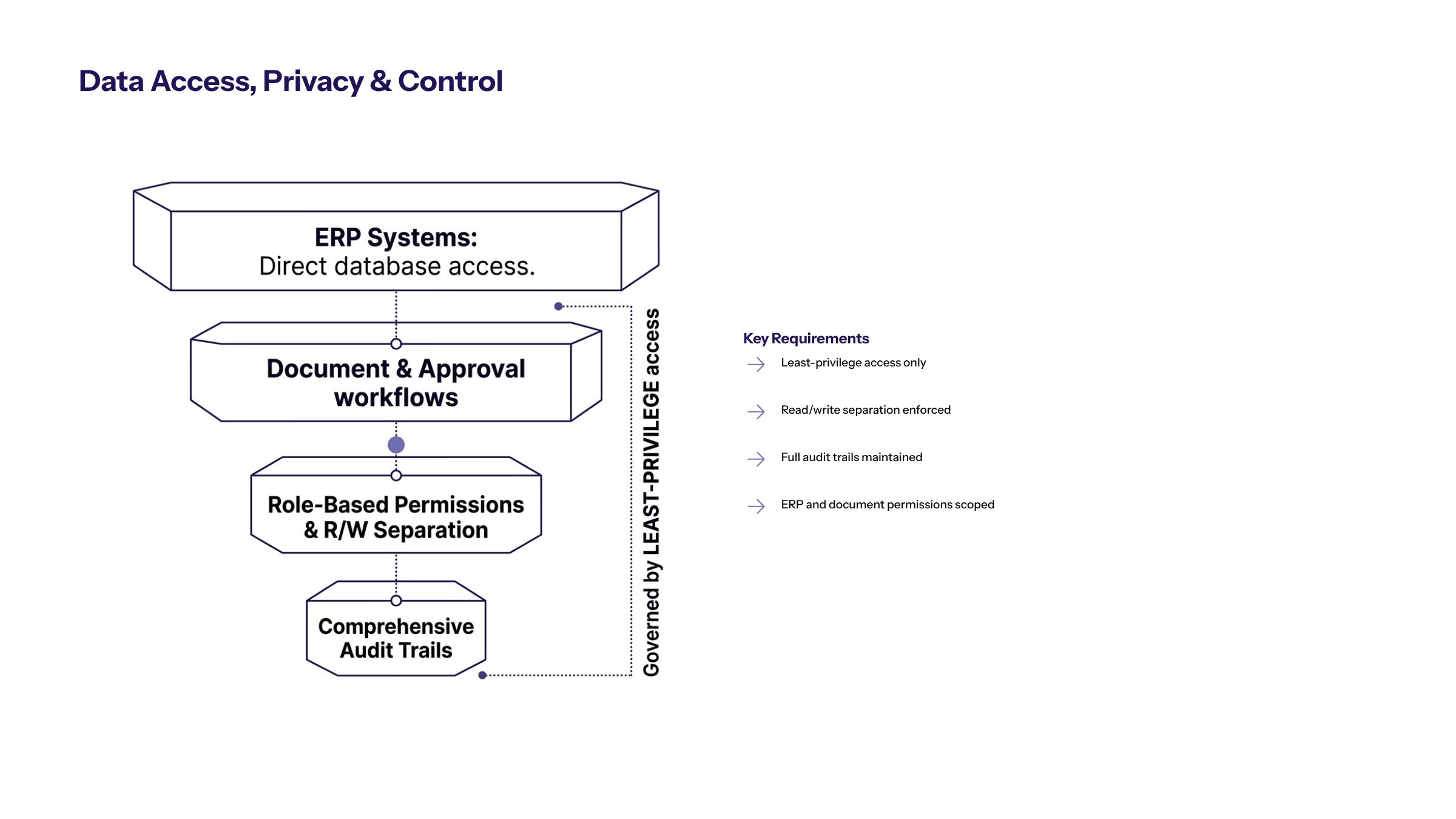

Data Access, Privacy, and Control Requirements

Data access should be specific. An AI workflow does not need broad access to every finance record. It needs approved access to the sources required for the workflow role. A document-review workflow may need document fields and vendor records. A reporting workflow may need structured inputs and approved commentary sources.

Secure development for finance workflow automation includes least-privilege permissions, role-based access, logging, input validation, output review, monitoring, and rollback planning. These controls should be part of the workflow design, not added after the pilot.

Privacy controls should address data minimization, retention, user access, and source visibility. Teams should know what data the AI system reads, where outputs are stored, who can view them, and how long they are retained. If external tools or model services are involved, data handling should be reviewed before production use.

Control requirements should also distinguish read, recommend, draft, route, and write actions. A read-only summary has a different risk profile than a workflow that updates records. The action model should determine the review threshold.

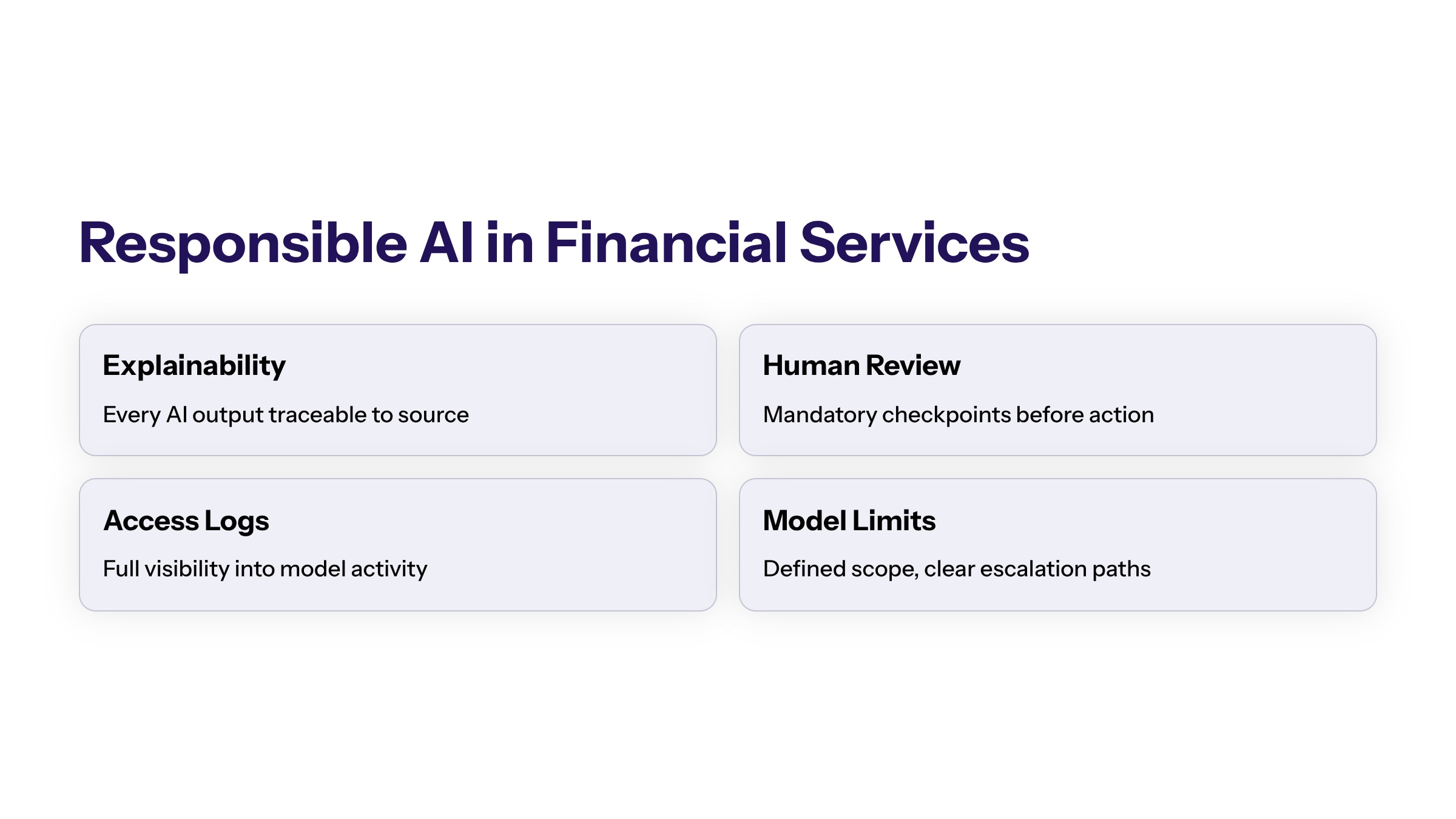

Responsible AI Implementation in Financial Services

Responsible AI implementation in financial services should be framed as governance and evidence design, not as a claim of compliance certification. Regulation-specific workflows should be reviewed by qualified business, legal, compliance, and risk owners before production use.

In practical workflow terms, responsible implementation means the team can explain who owns the workflow, what data is used, what action the AI can take, when a human reviews output, how exceptions are handled, and how evidence is retained. The system should support accountability.

Human review should be risk-based. Low-risk internal summaries may need lighter review than financial approvals, customer-impacting actions, or reporting-related workflows. High-risk actions should have defined approval thresholds and audit trails.

Monitoring should include both performance and control metrics. A workflow that reduces manual effort but creates unclear evidence is not ready for scale. Responsible implementation should measure workflow value and workflow trust together.

AI Agents Implementation in Financial Services

AI agents implementation in financial services should begin with bounded roles. A finance agent might retrieve context, summarize records, prepare review notes, classify documents, or route exceptions. It should not receive broad authority without clear permissions, review thresholds, and rollback paths.

Agent workflows need action inventories. List what the agent can read, what it can recommend, what it can draft, what it can route, and what it is not allowed to do. Then assign controls to each action type. This prevents agent automation from becoming unclear or overly permissive.

AI-first architecture helps define the system around finance agents: data access, retrieval, APIs, workflow engine, permissions, audit logs, monitoring, and human review. Architecture is where responsible AI principles become enforceable workflow behavior.

Finance teams should also define support ownership. If an agent fails, routes an exception incorrectly, or produces a questionable recommendation, someone needs responsibility for review and correction. Support ownership is part of production readiness.

Implementation Roadmap for Finance Workflow Automation

A finance workflow automation roadmap should start small and controlled. Choose one workflow with clear volume, clear ownership, and measurable friction. Avoid starting with broad autonomous finance operations.

Map the finance workflow. Document inputs, systems, owners, approvals, exceptions, and outputs.

Classify data and actions. Decide what data is needed and whether AI will read, recommend, draft, route, or write.

Define review thresholds. Set human approval rules based on risk and business impact.

Design evidence capture. Log inputs, outputs, actions, reviewers, overrides, and final workflow state.

Pilot with real variation. Test normal cases, exceptions, missing data, and ambiguous inputs.

Scale based on evidence. Expand only when the workflow is useful, secure, adopted, and reviewable.

Measuring Finance Workflow Automation

Measurement should focus on workflow outcomes and control quality. Useful workflow metrics include cycle time, queue age, manual touches, rework, approval latency, exception volume, and time to assignment. Useful control metrics include audit completeness, review rate, override frequency, permission failures, and unresolved exceptions.

Finance teams should avoid unsupported claims about savings or performance unless they have a sourced baseline and measured outcomes. A safer and more useful approach is to define what will be measured before the pilot begins.

Audit readiness should be considered as part of value. If automation makes the workflow faster but harder to reconstruct, the system may create risk. A stronger workflow improves visibility and evidence as well as speed.

Operating Model for Finance AI Workflows

Finance AI workflows need clear operating ownership after launch. The team should define who owns workflow performance, who reviews exceptions, who approves changes to data sources, who manages access, and who responds if automation behaves unexpectedly.

The operating model should include change control. A new approval rule, data source, prompt, model configuration, or integration can affect finance workflow behavior. Production changes should be documented, tested, reviewed, and rolled out according to risk.

Support should include both technical and business owners. The technical owner can manage integrations, logs, monitoring, and system reliability. The finance owner can confirm whether the workflow still fits business rules and whether exceptions are being handled correctly.

Periodic review should compare workflow metrics and control metrics. If cycle time improves but overrides rise sharply, the workflow may need better rules. If audit evidence is incomplete, the automation should not scale until the gap is fixed.

Finance Readiness Checklist

Before a finance AI workflow moves into pilot, the team should confirm the workflow owner, data owner, approval owner, technical owner, and escalation owner. Finance workflows often cross systems and departments, so ownership must be explicit before automation begins.

The team should also confirm that required records are accessible, source quality is acceptable, permissions are limited, and review thresholds are documented. If AI will prepare recommendations, the workflow should explain who reviews them. If AI will update workflow status, the system should log the update and allow correction.

This readiness check keeps finance workflow automation focused on support, visibility, and evidence. It avoids overstating AI autonomy in areas where accountability matters.

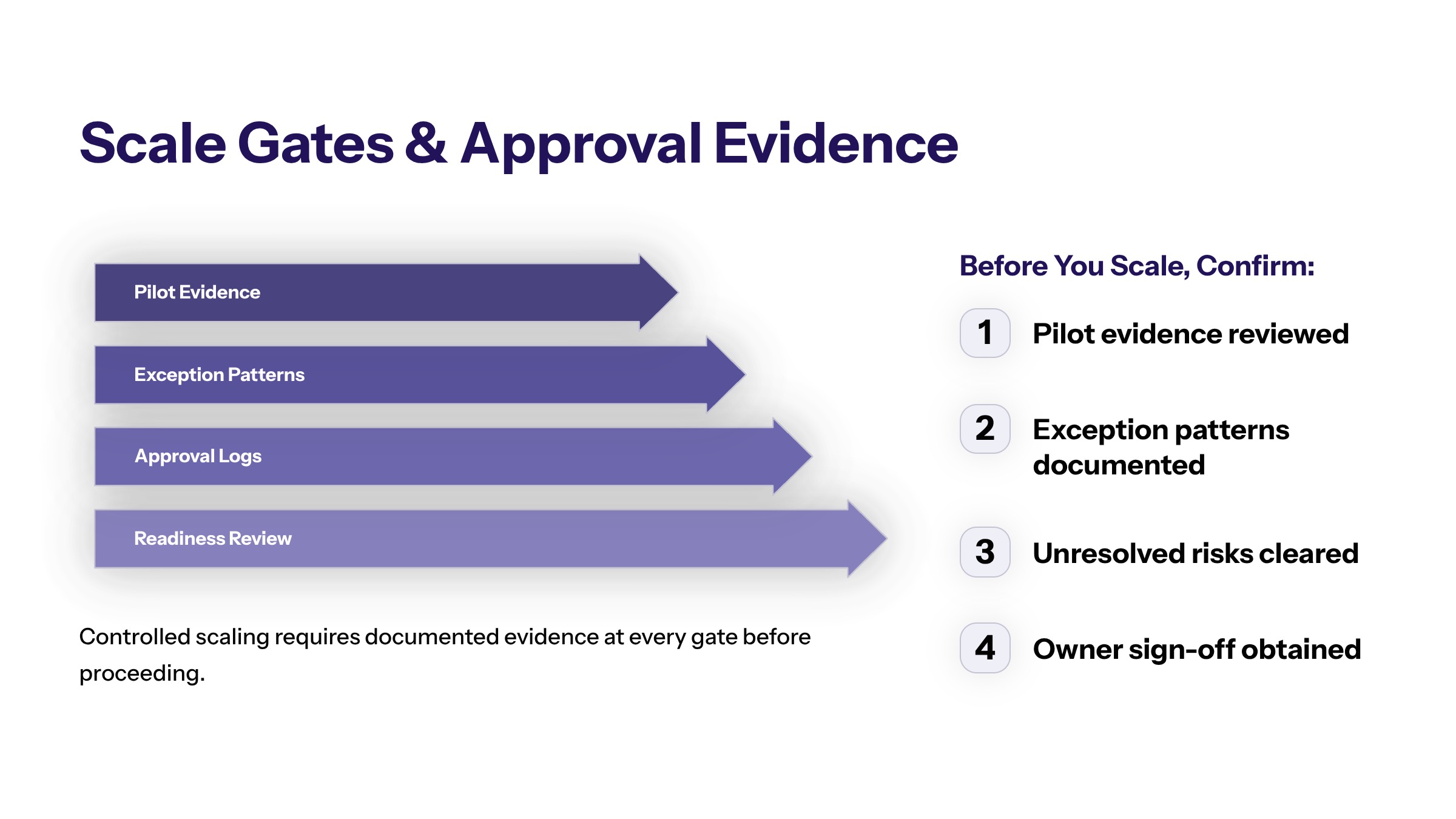

Finance Scale Gates and Approval Evidence

Finance AI workflows should scale only when the pilot shows both operational value and control quality. A workflow may be faster, but it should also be reviewable, permissioned, and easy to explain. If the audit trail is weak or approvals are unclear, the workflow should remain limited.

Decision gates should define what evidence is required for expansion. That may include stable exception handling, complete logs, acceptable override patterns, clear owner feedback, and reliable system integration. These gates help finance teams avoid expanding automation based only on early enthusiasm.

The decision should also consider support readiness. If the finance team cannot explain who owns exceptions, access reviews, workflow changes, and incident response, the automation should remain in pilot until ownership is resolved.

This protects finance teams from scaling a workflow that looks efficient but cannot be governed. It also gives leadership a clearer basis for approving the next stage. Finance automation should earn broader access through evidence, not assumption.

That evidence should be understandable to finance, technology, and risk stakeholders before expansion. The gate should show what the AI system did, what it did not do, who reviewed the output, which records were used, which exceptions remained unresolved, and why the next stage is justified. That level of evidence keeps the decision tied to control quality instead of enthusiasm for automation.

How to Start Finance Workflow Automation

AI workflow automation for finance should be implemented with control first. Start by selecting one workflow, mapping the data and approvals, defining the AI role, and setting review thresholds before production use.

The best finance automation programs use AI to support better workflow visibility, cleaner handoffs, and stronger evidence. They do not remove accountability from finance decisions.

Frequently Asked Questions About AI Workflow Automation for Finance: Use Cases, Controls, and Implementation

High-impact finance actions should not be automated without clear approval thresholds, controls, and review. Many teams start with AI support for review, routing, and exception preparation rather than autonomous action. For related reading, see generative AI development.

No. Finance and regulated-industry workflows require appropriate professional judgment from qualified internal owners. AI can support workflow design, controls, and implementation planning, but it should not replace accountable review. For related reading, see AI and ML development.

Start with a bounded workflow such as document classification, invoice review support, exception routing, or reporting note preparation where the owner, data, and review path are clear. For related reading, see AI implementation planning.

Payments, approvals, vendor changes, account updates, and policy exceptions should require human approval. AI can prepare review packets, but high impact finance actions need accountable signoff. For related reading, see AI automation services.

Finance teams should keep evidence of inputs, retrieved records, AI outputs, review decisions, approvals, actions, and exceptions. Auditability is essential when automation touches financial controls. For related reading, see enterprise AI services.

Missing purchase orders, inconsistent vendor records, duplicate invoices, unclear approval rules, and outdated policy data can weaken finance automation. Data quality should be reviewed before execution is expanded. For related reading, see AI consulting services.